10 Charts: Macro data keeps confirming our view.

Big Picture

💡 Macro keeps firming up across labor, consumer, and inflation. Earnings say the same thing.

Ok so busy week and busy month really with market gyrating daily on headlines. Funny though with the noise, the macro continues to hold up and improve. Another week of supportive data reinforces our view that peak uncertainty is behind us and the longer-term backdrop remains healthy. We’ve been beating this drum for a while. Sometimes doesn’t feel like it but it is the right move to stay pat.

Retail sales this past week came in around +1.9% ex-autos, beating estimates and extending a run of resilient prints. The ADP weekly pulse 4-week moving average took another leg higher to +55K, now 5 straight weeks of improvement. Initial claims held in the low 210s. The S&P Global US Composite PMI rebounded to 52.0, a 3-month high. Different data sources, same read for the most part, ie the economy is on solid footing, something we have not backed away from.

Earnings season kept reinforcing it. Tesla printed a mixed quarter but margins expanded nicely to 21.1%, which we liked. ServiceNow had really healthy numbers. Subscription revenue up 22% Y/Y with cRPO +21% constant currency, and the AI target for the year got raised from $1B to $1.5B. The market sold it off on the margin guide (maybe or just SAAS jitters). Our belief continues to be that the large software platforms central to mission-critical operations, with technical ability at the top, execute well in this environment.

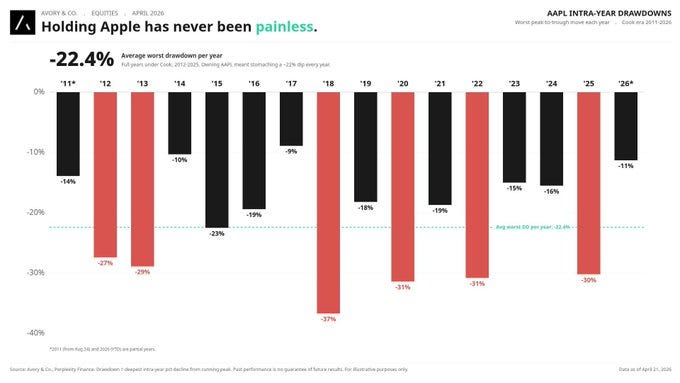

We also said goodbye to Tim Cook. Incredible career, roughly 2000% total return under his watch. Worth remembering what it took to earn that return though, on avg Apple stock was down 24% a year at some point with Cook at the helm. Patience and stomach are part of the equation, forsure.

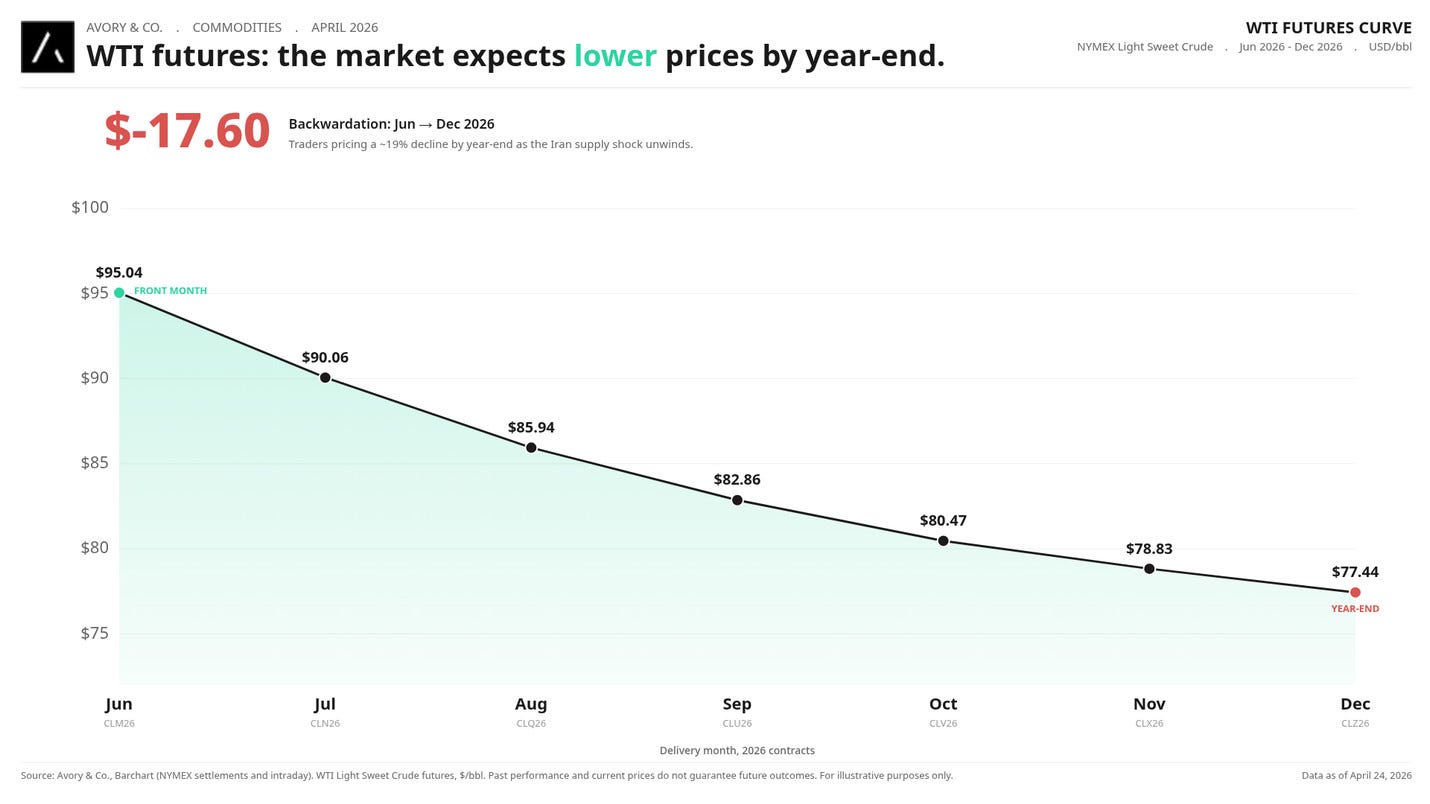

We remain constructive. Consumer is in good shape, jobs market is building momentum, inflation dynamics remain absorbable (rent disinflation keeps grinding lower), and guidance is good enough right now. WTI futures currently price mid-to-high 70s by year-end. Moving target, but directionally consistent with conflict easing over time. That’s the read from our desk.

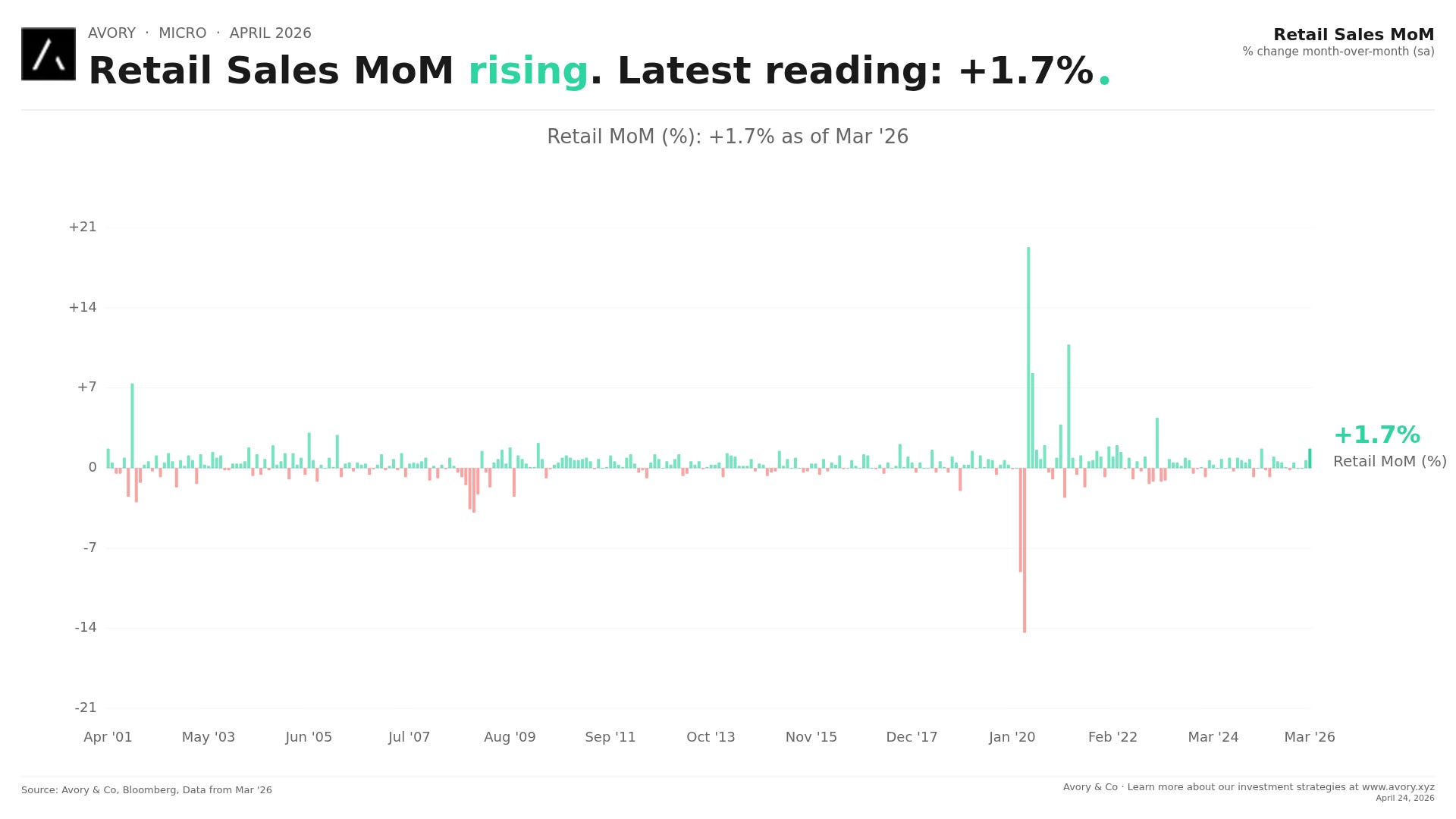

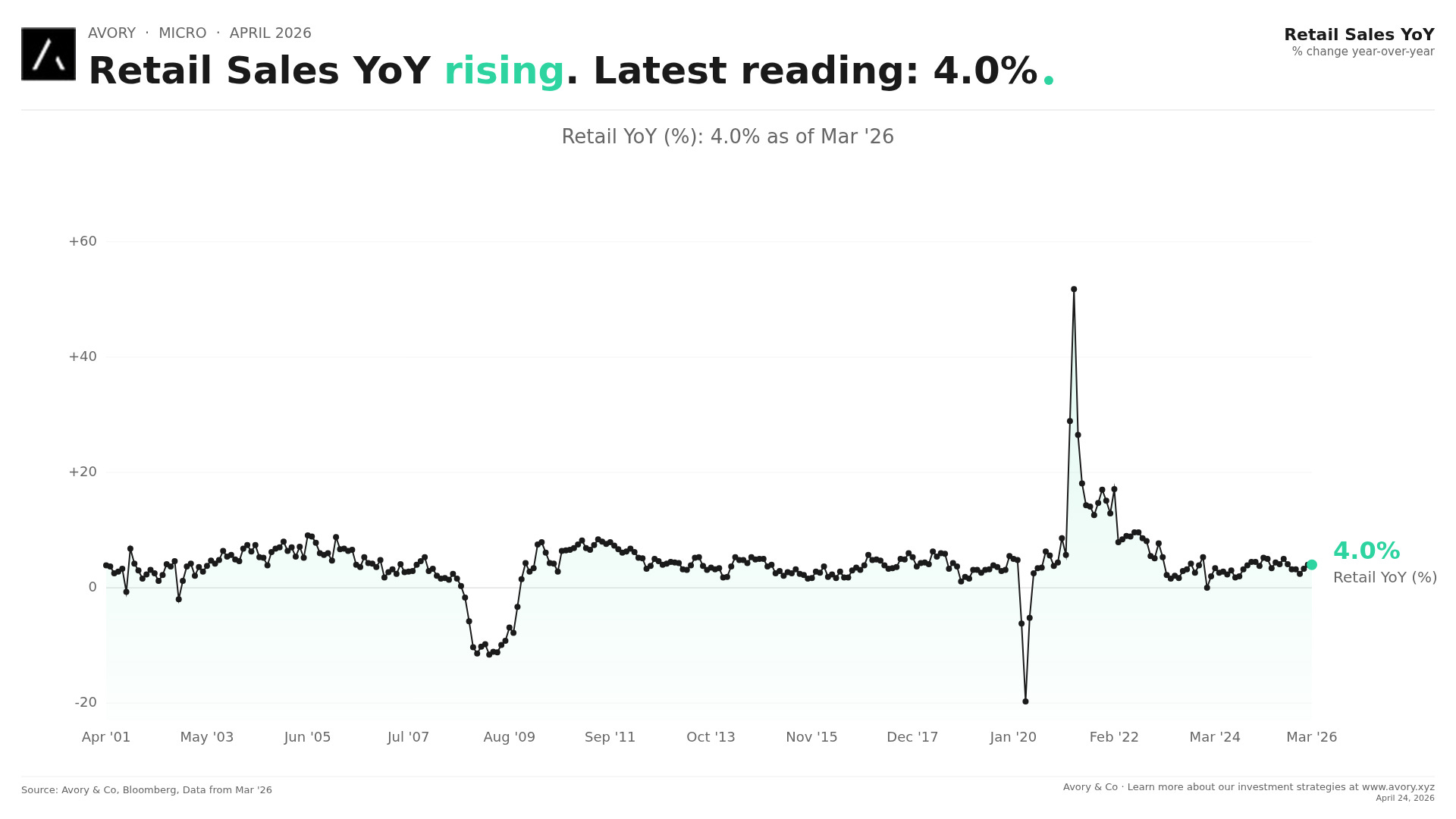

[1] Retail sales +1.7%, +1.9% ex-autos. Hard to say weak consumer.

Lets start with the March retail sales data that came in at +1.7% M/M headline vs. +1.4% expected. Ex-autos hit +1.9% vs. +1.3% expected. 12 of 13 categories were up, the most in months. That follows an upwardly revised +0.7% in February.

The consumer keeps spending because the consumer has money. Tax refunds are tracking ~10-15% Y/Y and hiring has picked up. This is what “good enough” looks like. That’ll do.

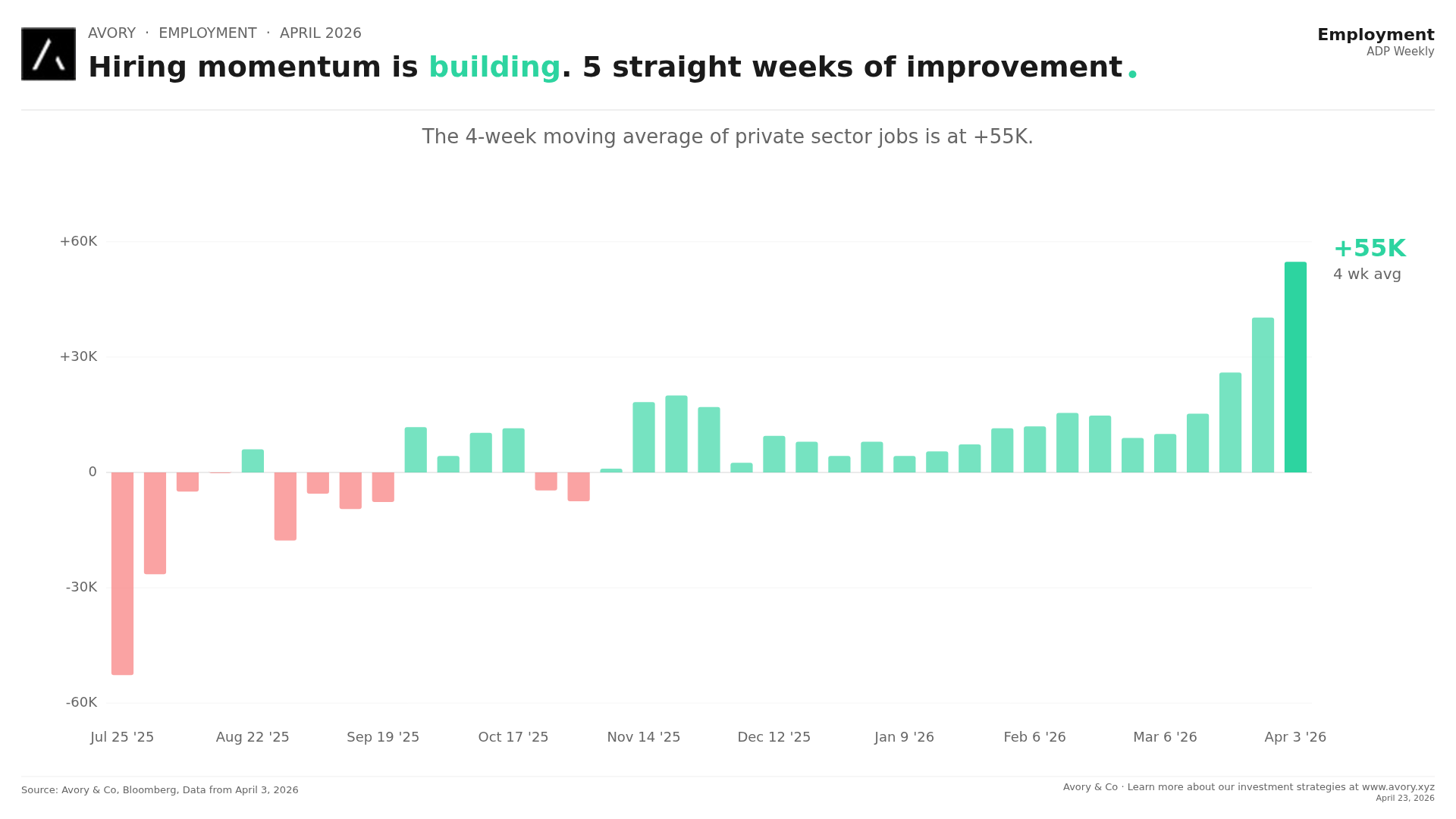

[2] Hiring momentum is building. 5 straight weeks of improvement. Oops more strength…

The ADP weekly pulse 4-week moving average hit +55K private sector jobs. That’s the 5th consecutive week of acceleration.

To put that in context, this number was sitting near zero through most of the fall. It has inflected meaningfully in a short window. The labor market is firming here????

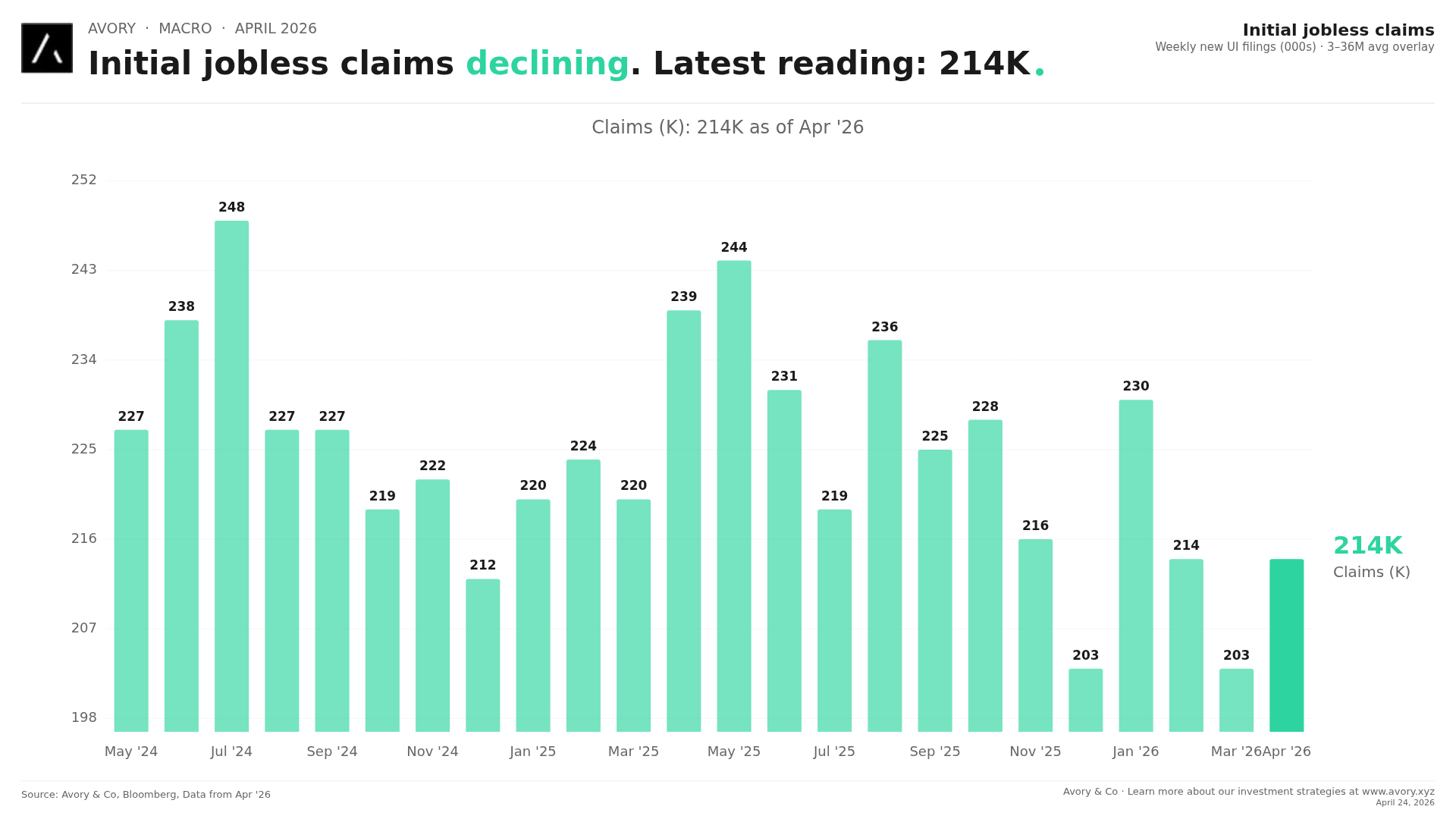

[3] Initial claims in the low 210s. No crack in the labor market.

Initial jobless claims printed 214K for the week ending April 18. The prior week was 208K. We are sitting in a range that historically correlates with a healthy labor market.

Combine this with ADP accelerating and you get a consistent message. Hiring is picking up and firing is not picking up. Not bad

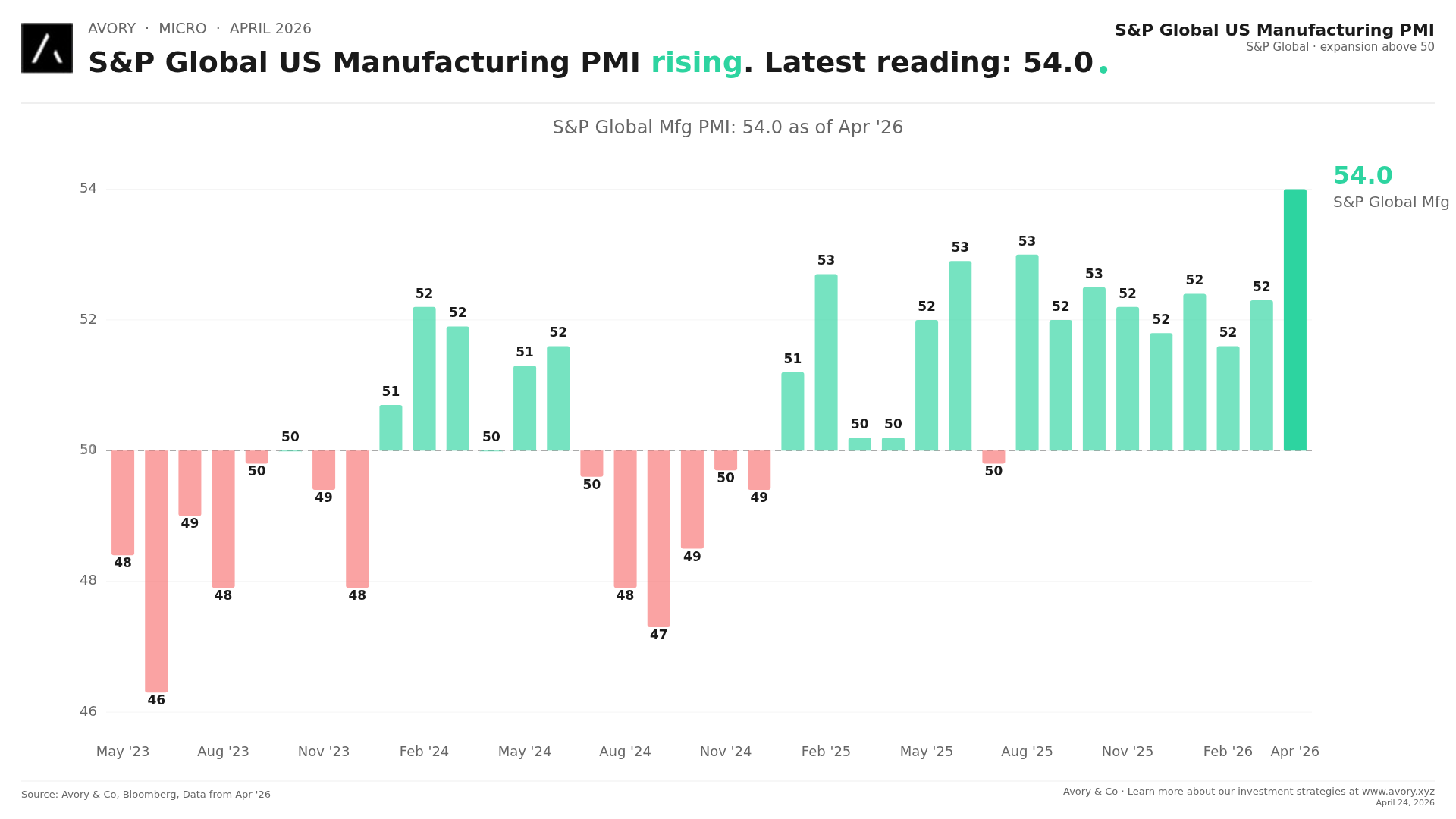

[4] S&P Global US Manufacturing PMI Highest in a LONG TIME.

The flash Composite Output Index went from 50.3 in March (a 2.5-year low) to 52.0 in April. Manufacturing PMI hit 54.0, the highest since May 2022. Services moved back to 51.3.

Activity growth rebounded as we kicked off Q2. Another data point pointing the same direction as retail sales and ADP. The economy is on a solid foundation. Checks the box for us.

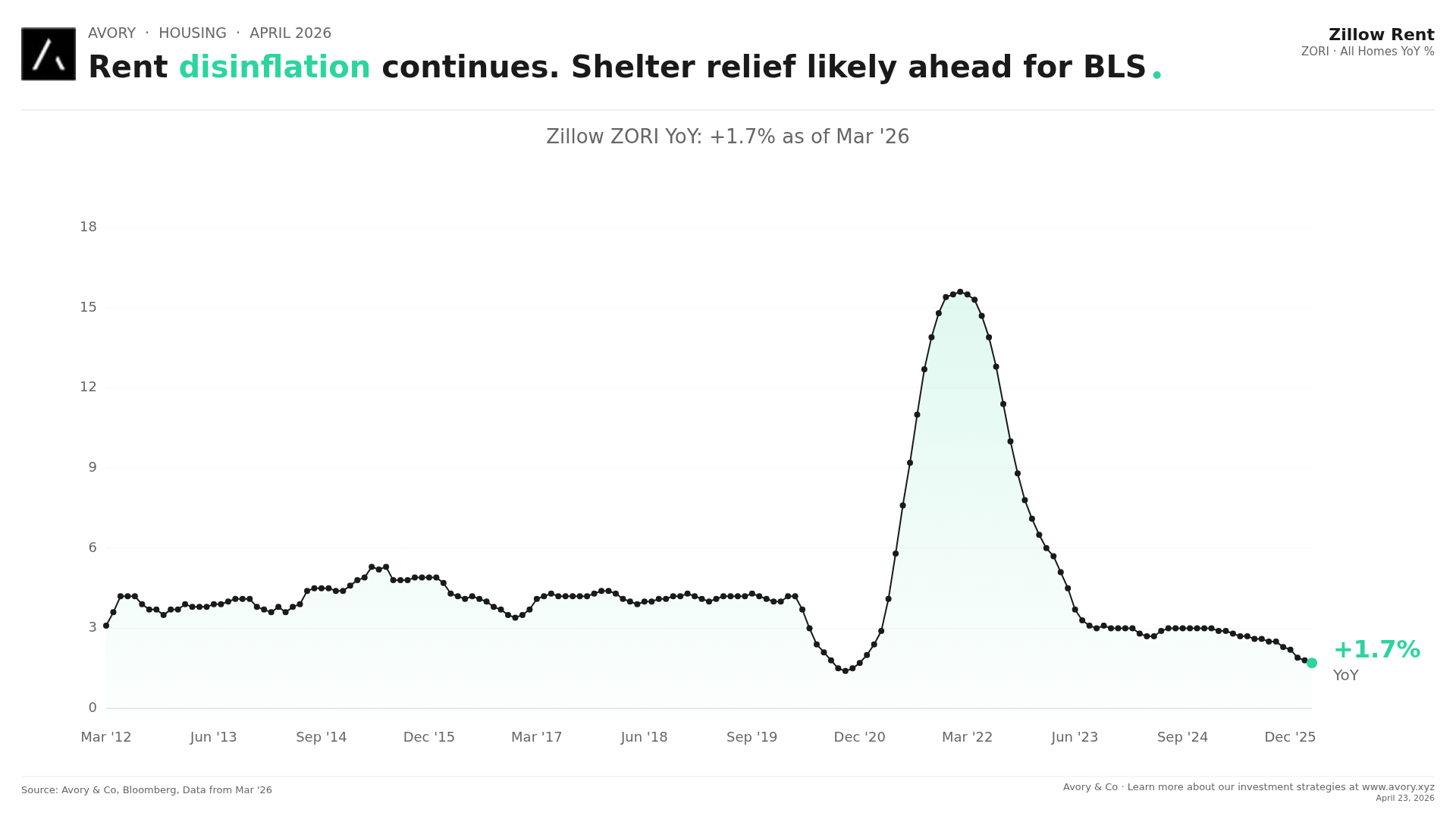

[5] Rent disinflation continues. +1.7% Y/Y.

Zillow’s Rent Index grew just +1.7% Y/Y as of March. That compares to the +15%+ peak in early 2022. This is well below the pre-COVID average of ~3-4%.

Shelter is the single largest weight in CPI. The BLS methodology lags private market data by 6-12 months. So what shows up in today’s Zillow print is likely to flow into official inflation data over the next several quarters. This is disinflationary fuel that has not fully shown up yet.

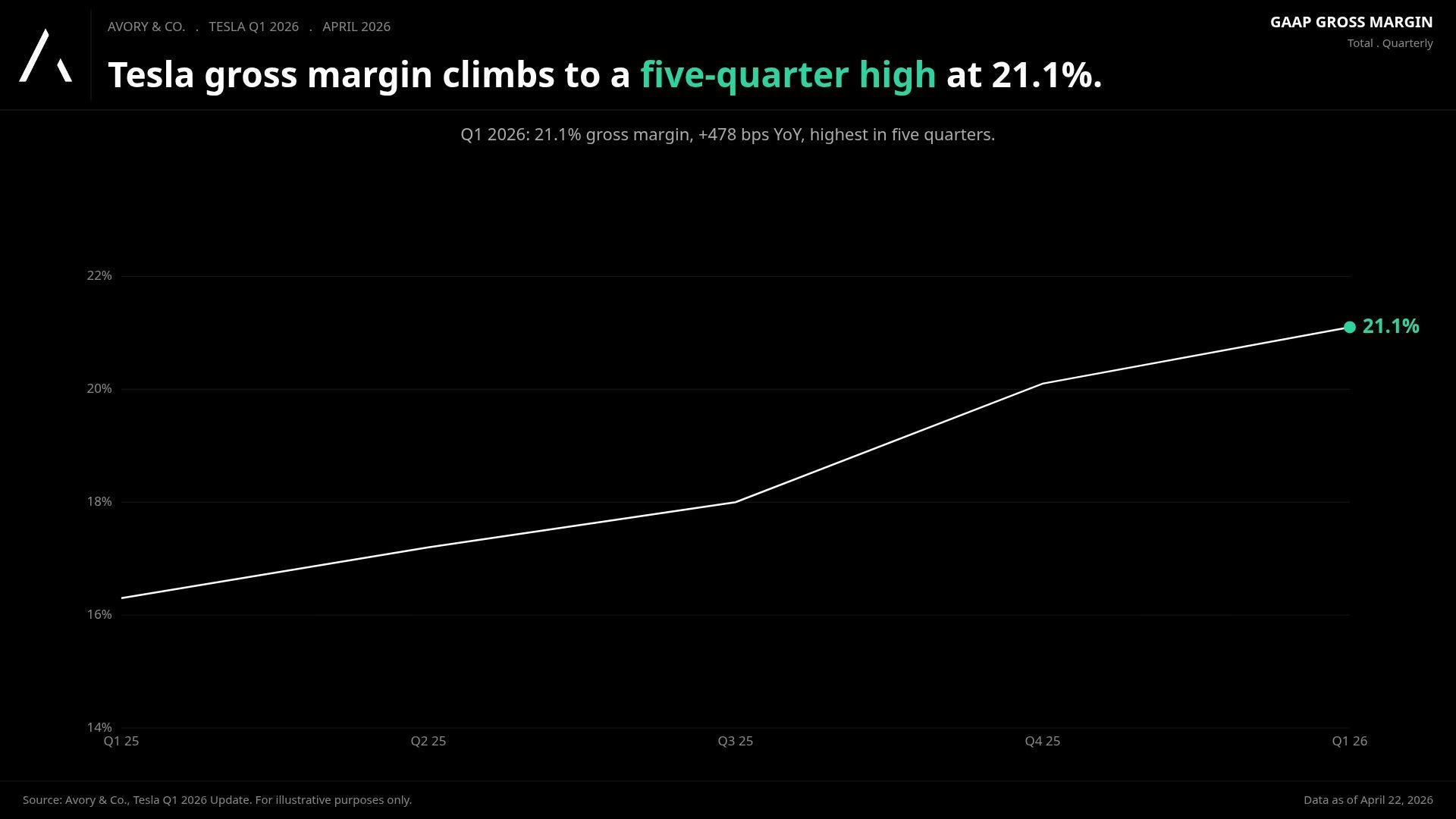

[6] Tesla margins expanded. 21.1% total gross margin.

Tesla reported Q1. Revenue +16% Y/Y to $22.4B, EPS of $0.41 vs. $0.36 expected. The headline was the margin line: total gross margin 21.1%, up from 16.3% in Q1 2025. Auto gross margin ex-credits improved sequentially to 19.2%.

Mixed quarter overall. Deliveries missed and some of the margin lift came from one-time benefits. But in the grand scheme of things, constructive. We care about the direction of margins and that direction was up. Can’t complain about that.

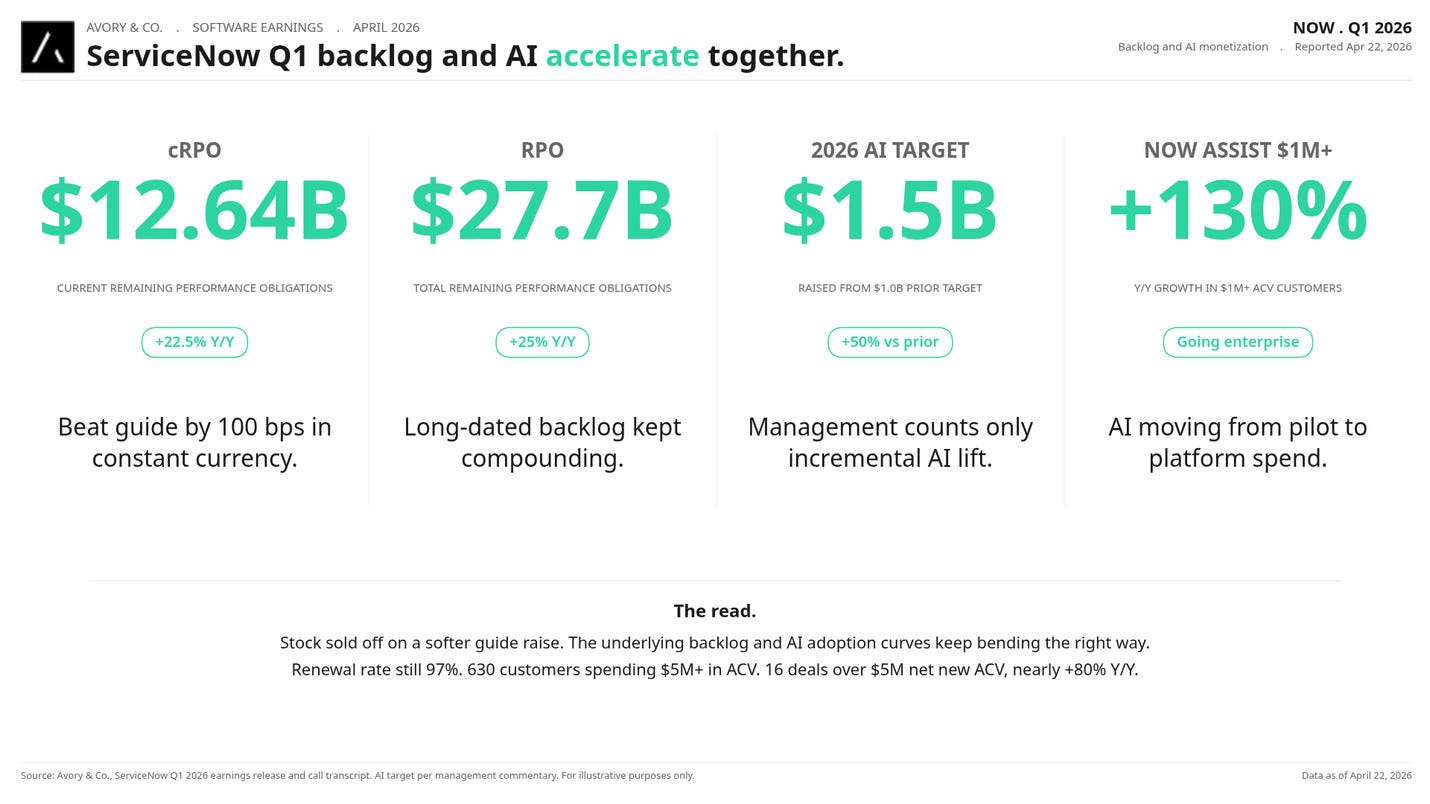

[7] ServiceNow had a really strong quarter. Market didn’t love the guide apparently.

Subscription revenue $3.67B, up +22% Y/Y (+19% constant currency). cRPO $12.64B, +21% constant currency. Beat guide by 100bps. Non-GAAP operating margin 32.0%, beat by 50bps. FCF margin hit 44%.

Biggest tell for us: the internal 2026 AI target moved from $1.0B to $1.5B, same measurement methodology. Customers with >$1M on Now Assist grew +130% Y/Y. Deals with 3+ Now Assist products grew ~70%.

Stock NOW 0.00%↑ sold off ~12% after hours on a softer margin guide that includes Armis dilution. That is the debate. Our read: demand side of the business is accelerating, AI is converting. Mission-critical software platforms with strong leadership keep executing in this environment. This is one we may want to own.

[8] Tim Cook retires. ~2000% return during his tenure BUT Avg 22% drawdown.

Tim Cook announced he will step down Sept 1. John Ternus takes over. Under Cook, Apple market cap went from ~$350B to $4T. Annual revenue roughly quadrupled from $108B in 2011 to $416B in 2025.

What is interesting though is what it took to earn that return. The chart we built this week shows the average and max drawdowns along the way. The run wasn’t straight up. Patience and stomach are always part of the equation. Great operator, great run.

[9] WTI futures curve: mid-to-high 70s by year-end.

The WTI futures strip is currently pricing the mid-to-high 70s by year-end. Moving target, but the curve continues to reflect the market’s expectation that conflict pressure eases over time.

The daily tell for us remains the front-month. Every week without escalation slowly repricing what has been a big source of uncertainty since February. Watching closely.

Looking Ahead

Earnings acceleration. Big Tech next week. We want to see whether AI features are converting to software revenue in the same way ServiceNow showed us this week despite getting hit.

Conflict resolution. Every week without escalation changes the probability table. Oil futures remain the daily tell.

Breadth. Still thin. We want to see more stocks participate in the ATH.

Fed speak. Watch for commentary on the Composite PMI rebound and whether it shifts the tone. Lets see…

That’s all for this week!

Know another investor who'd find this useful? Forward it along or share on your page!About Avory & Co.

Investing Forward.

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn’t constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us:

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube": Channel

🎙️ Avory: Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.