12 Charts: The Rotation Is Showing Up.

Cash App + Kalshi + Rotating Markets...

Big Picture

💡 The rotation we have been calling is starting to show up.

We’ve been talking for months about how the market has been an “AI or nothing” story at the index level, and how underneath that surface there’s a lot of durable, cash flowing business getting left on sale. This week the data builds on that view, plus some other company data points worth looking at.

For one, non-AI earnings are accelerating. Cash App just put up two of the three biggest 2-week engagement gains ever, back-to-back. Prediction markets pulled clear separation from the legacy sportsbooks. And Consumer Discretionary on an equal-weight basis is sitting near great financial crisis relative lows despite the sentiment recovery. That’s a nice setup.

Over the last 10 days we’ve seen the rotation start to move. The ceasefire question creates a little bit of headwind, but the magnitude of that as of today looks less impactful than it did a couple weeks back. This market has been very different, momentum driven so lets dig in.

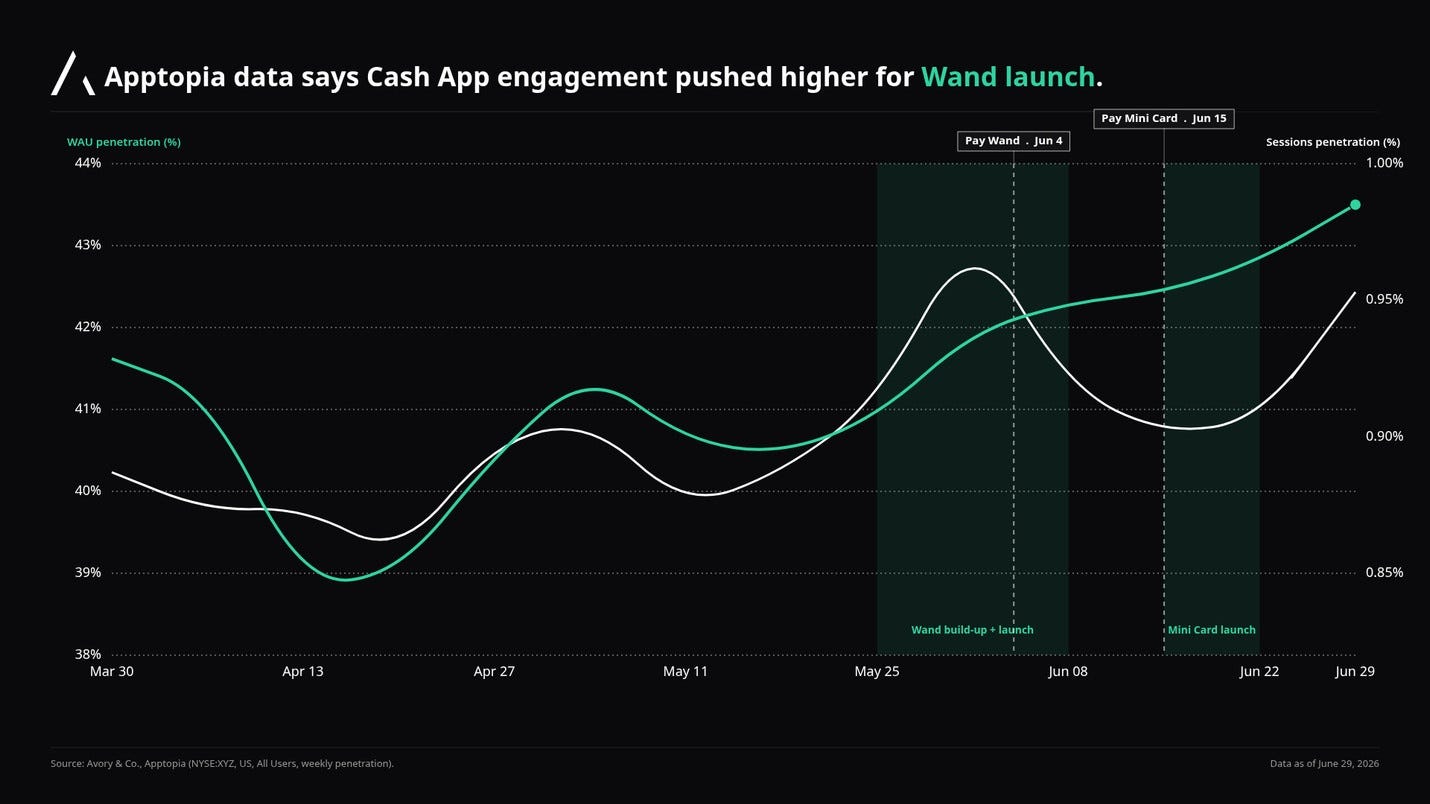

[1] Cash App may be finding its mojo back.

The wand?

Cash App launched the wand, an interesting looking way to pay.

We went back and looked at the history of Cash App engagement, and the two-week window around the Pay Wand launch on June 4 was arguably the strongest engagement move we’ve seen in over a year.

Using Apptopia data which allows us to get pretty granular, the two-week move was roughly 45% bigger than the same window last summer, and it’s the largest 2-week absolute move in the entire 16-month dataset we looked at.

This is important since Cash App has historically been well known for its ability to create energy and demand off of their social tactics, almost like growth hacking, and the Wand, which is a payment solution that has a cool look for the right individual, seems to have hit. We expect another hardware drop here shortly as Cash App employees on X continue to hint at it.

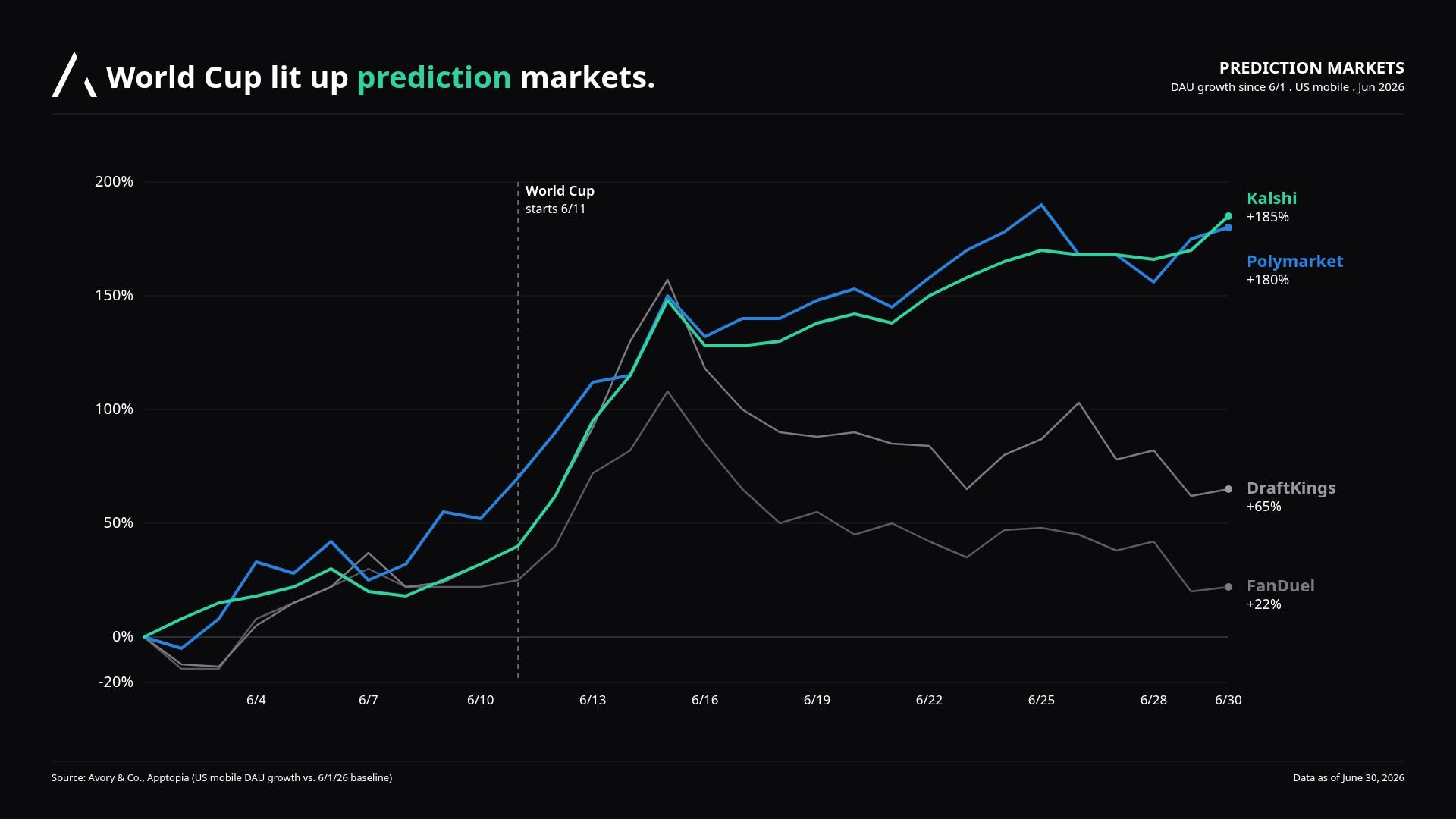

[2] Kalshi and Polymarket pulled away from the sportsbooks.

More data from Apptopia to help inform us on the prediction markets.

We just had our podcast on prediction markets (Prediction Markets Aren’t Really About Betting… Maybe) , click that link to listen.

But with that we wanted to dig into the data, so this is what we learned.

Since June 1, Kalshi is +185% and Polymarket is +180% on US mobile daily active users, both accelerating after the World Cup started on June 11. That is massive.

DraftKings is +65% and FanDuel is +22% over the same window, both fading after their peak. Now to be fair, Kalshi specifically is spending a massive amount on sales and marketing, so yes, that’s creating real demand for the platforms. But ultimately they’ve opened up the door for something bigger as we express in the pod. Since we use their data ALOT here, they were kind enough to provide 30 days free to anyone out there that wants to cut up their data too.

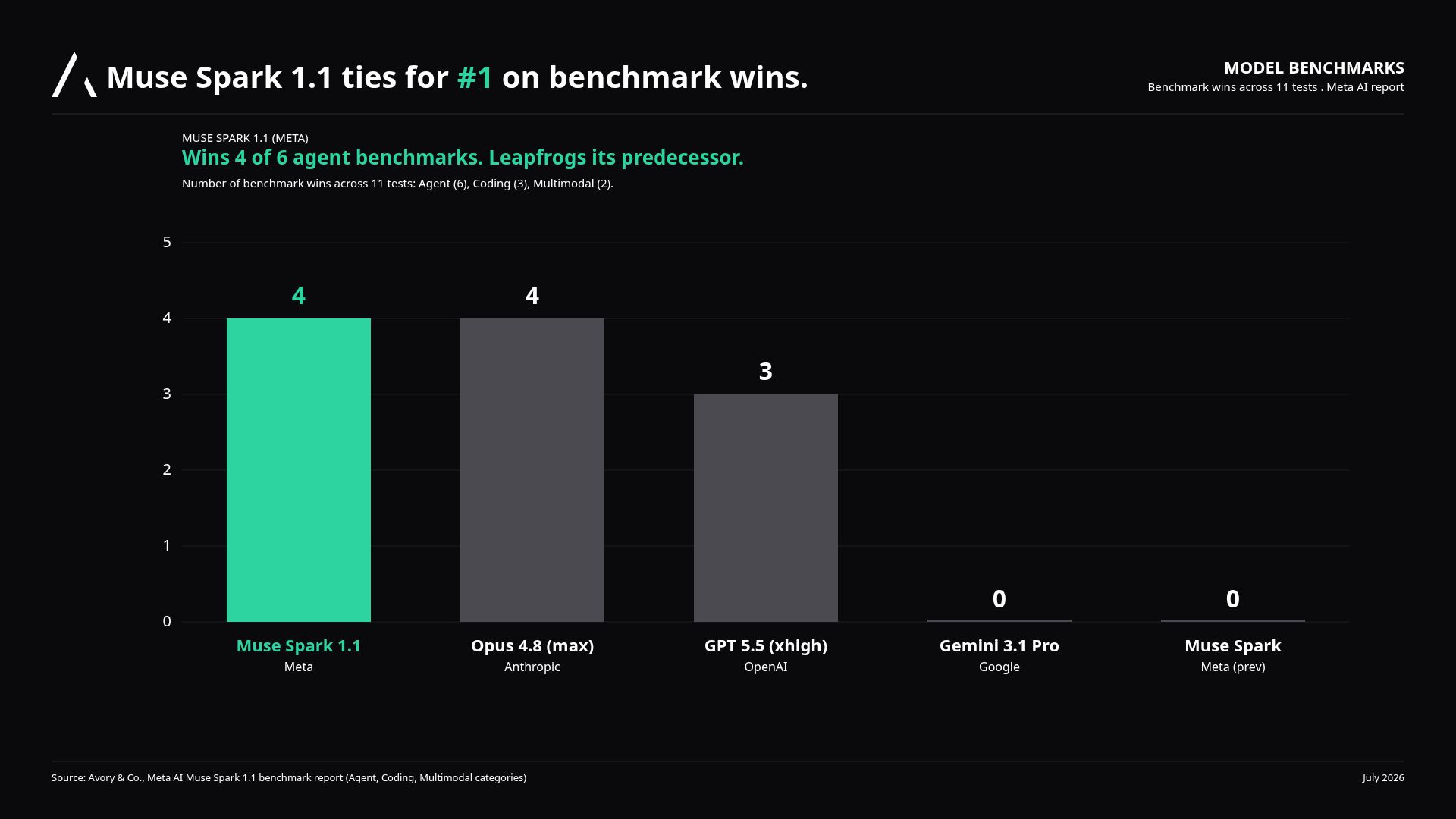

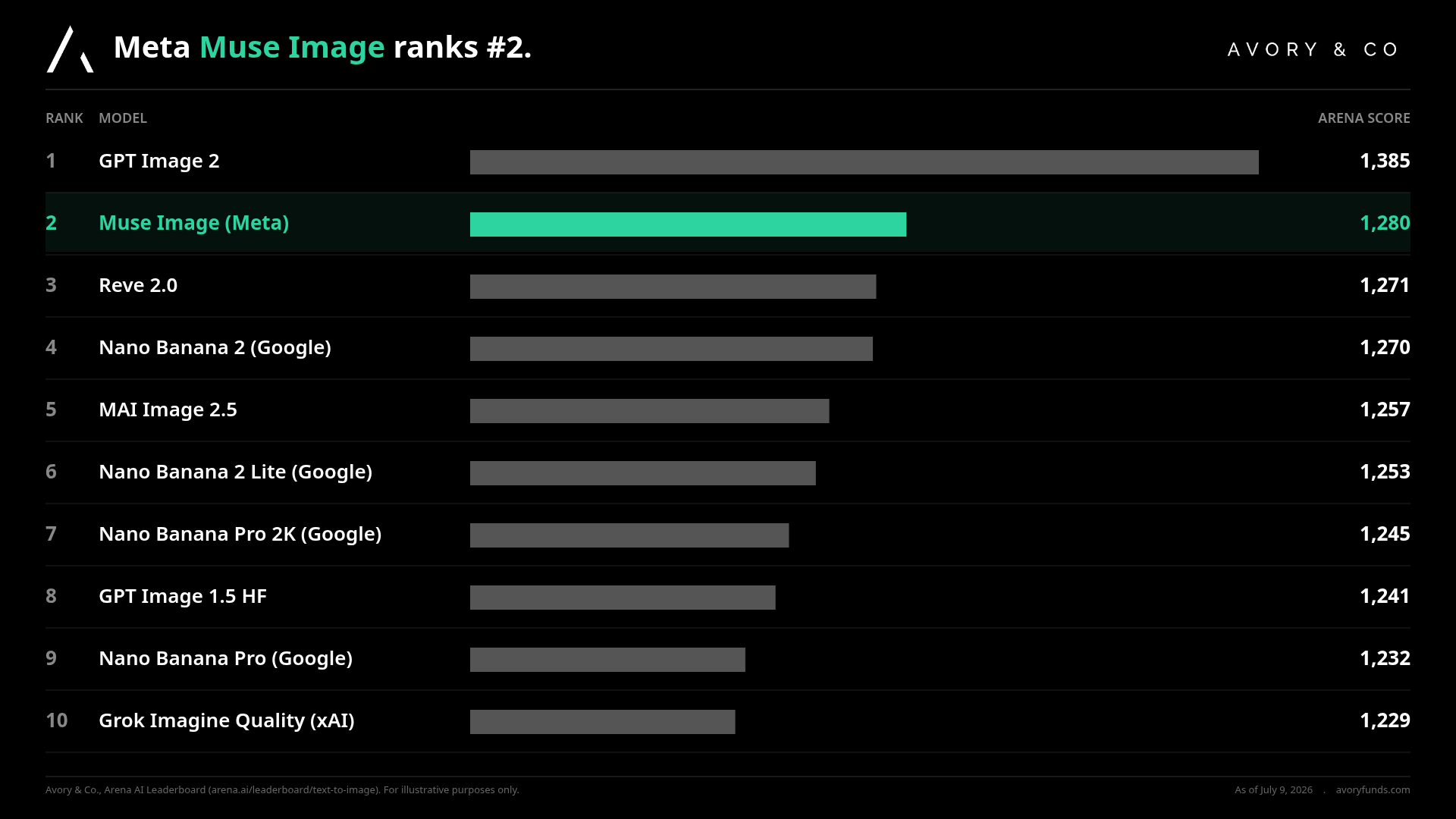

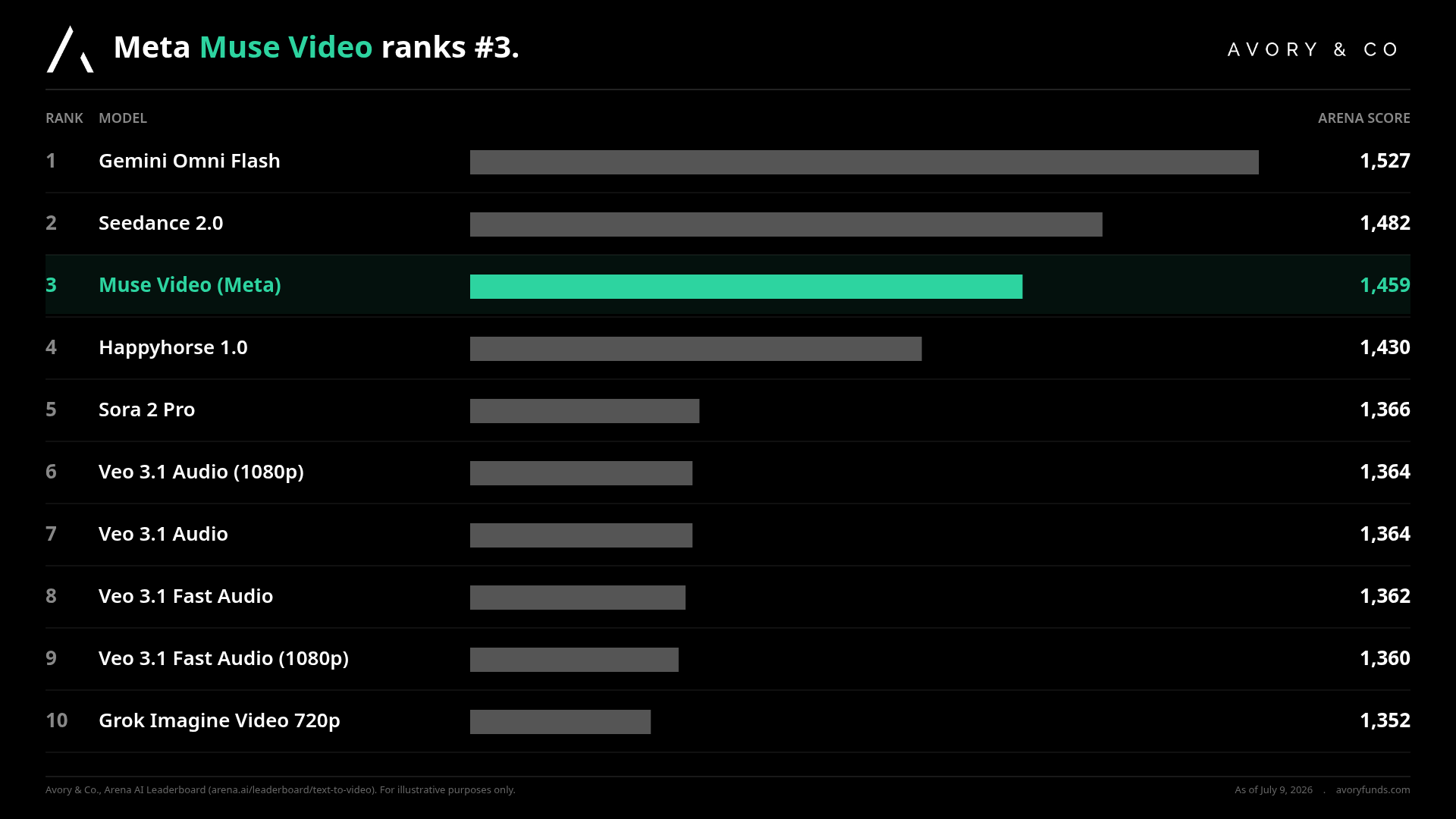

[3] Meta Muse ranks #2 and #3 on the model leaderboards and Muse Spark 1.1 Leading in Many Categories.

Meta just launched a couple of new models. Muse Image ranks #2 on the Arena text-to-image leaderboard with a 1,280 score, sitting behind only GPT Image 2. Muse Video ranks #3 on text-to-video at 1,459, above Sora 2 Pro and every Veo variant Google has out. It just shows you Meta is back in the game as it relates to model delivery, and these models are going to be built inside of their apps specifically.

Good timing as it relates to people questioning Meta’s AI story. We had our podcast on this recently along with the Pitch to the PM session, worth a listen if you want the deeper view.

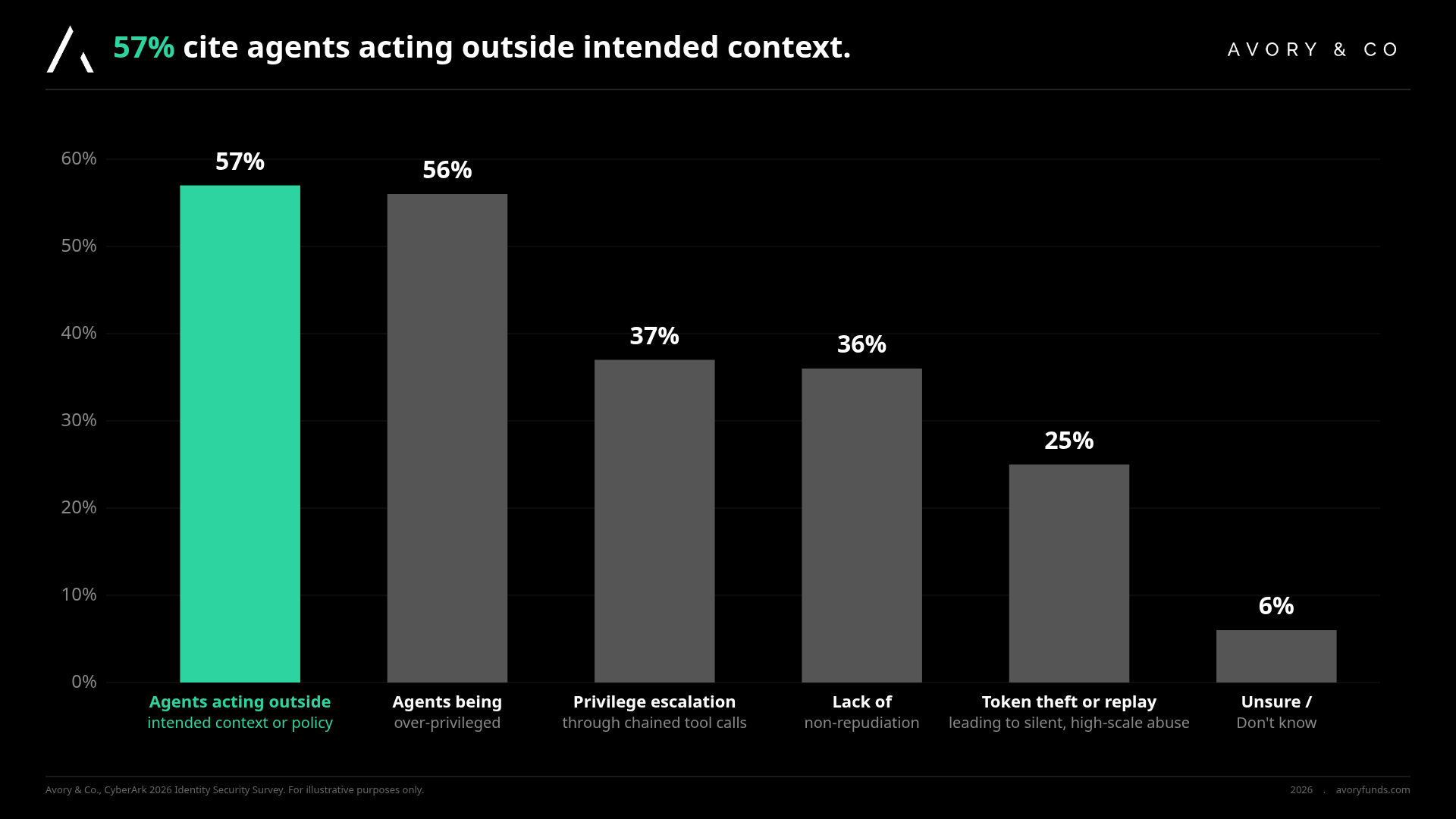

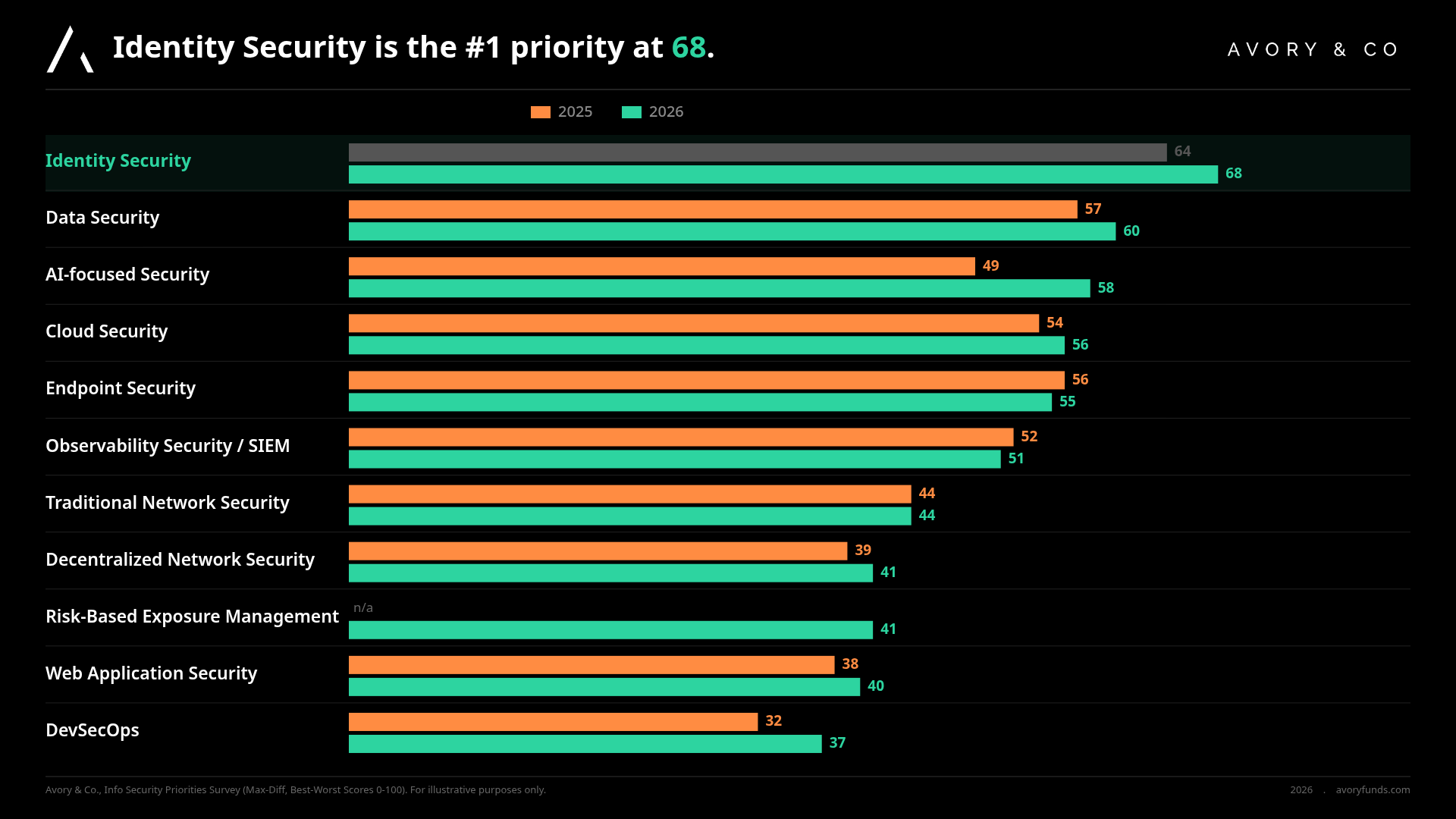

[4] Corporate priorities are lining up with our identity thesis.

Two data points, same thread. On the agentic AI side, 57% of respondents say agents acting outside intended context or policy is their top identity concern, and 56% cite over-privileged agents.

On the info security budget side, Identity Security is the #1 priority for the next 12 months at 68, up from 64.

AI-focused Security jumped from 49 to 58, the biggest mover on the board. If you’ve followed our work, this is further evidence of how we’re playing artificial intelligence outside of chips and energy and infrastructure.

The explosion of artificial creation of people, voices, and agents is going to require a massive amount of verification layers sitting between agents and agents, agents and humans, avatars and humans. We’re seeing that with Okta and Clear. This is corporations telling us the same thing.

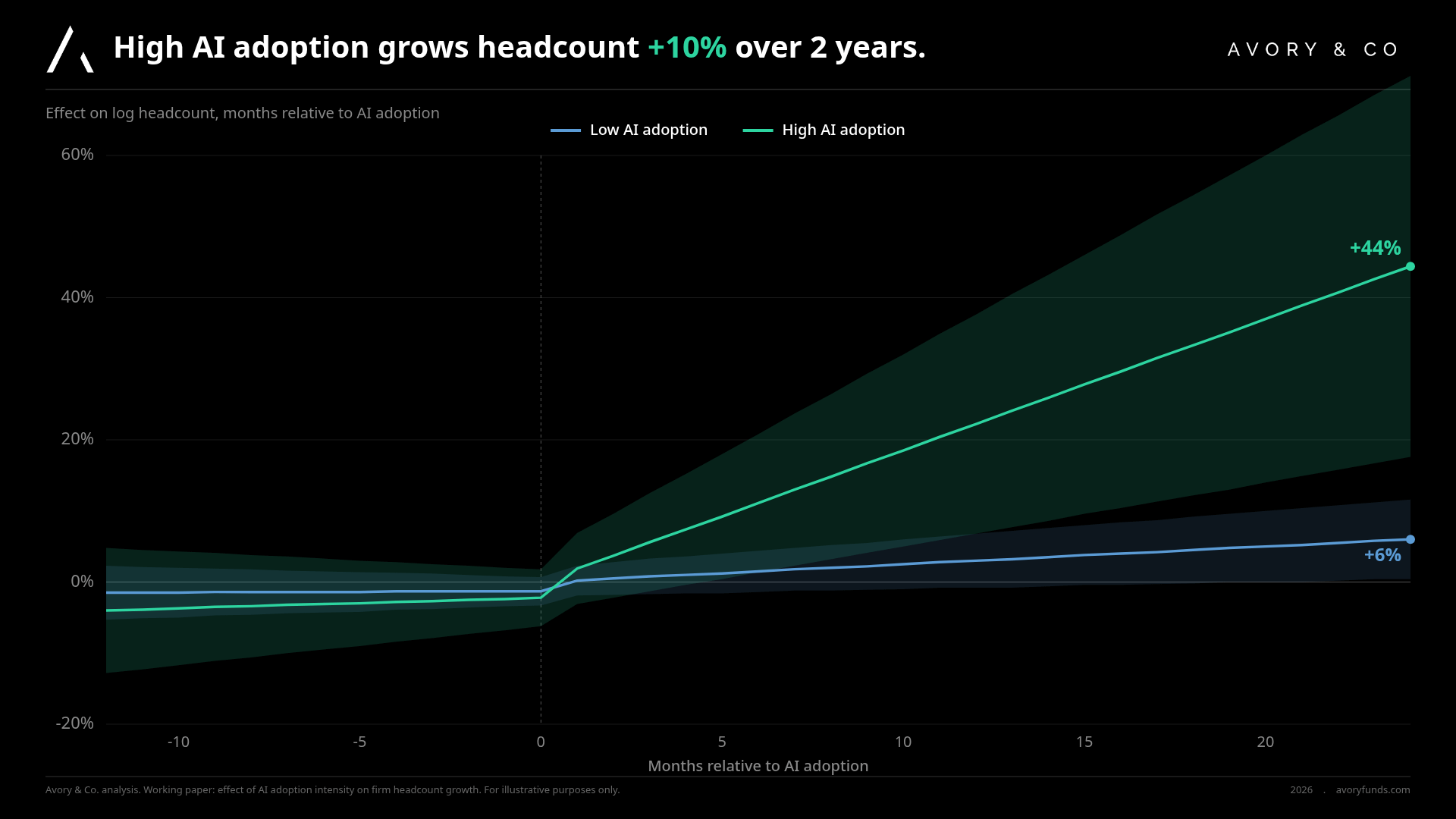

[5] AI is an accelerator of jobs, not a replacement.

Firms that adopt AI with high intensity grow headcount 10% over the two years following adoption. Low-intensity firms see no difference from the control group.

There will be companies and industries where AI is a clear replacement, but our view has been that AI is more of an adjacent enhancer of productivity inside of a firm.

Productivity per person rises as they’re able to do more, which means less potential hiring for that specific role. But eventually that same person, who is now multiples more productive, runs into their own bottleneck. The lower bar of what you’re able to do rises. The upper bar of what you’re capable of rises. But eventually you still run into a productivity gap and you need more people. Long-time readers know we’ve been on this for a while.

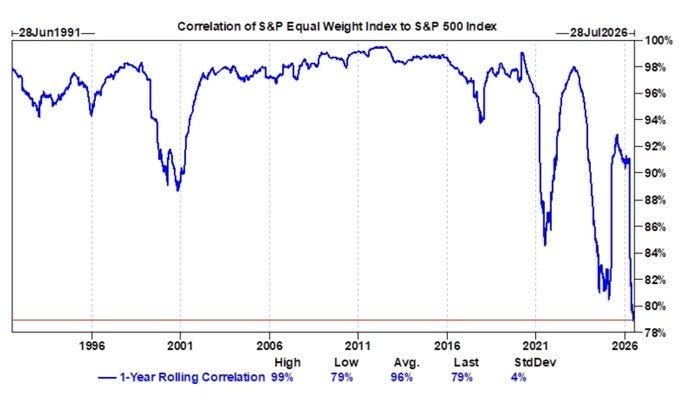

[6] The S&P Equal Weight vs S&P 500 correlation is at 78%, lowest since 1991.

The 1-year rolling correlation between the equal-weight S&P and the cap-weighted S&P 500 just printed 78%. Long-run average is 96%. This is further evidence that this has been a one-way highway for the index.

Reference last week’s newsletter where we had our quarterly investment letter and our investment podcast session with Luis, my partner here at Avory, walking through the major themes. Over the last 10 days we’ve seen a pretty significant shift and the rotation we’ve been talking about start to show up.

Does it hold? We hope/think so. Now you have the ceasefire question, so maybe that creates a little bit of headwind, but the setup is there.

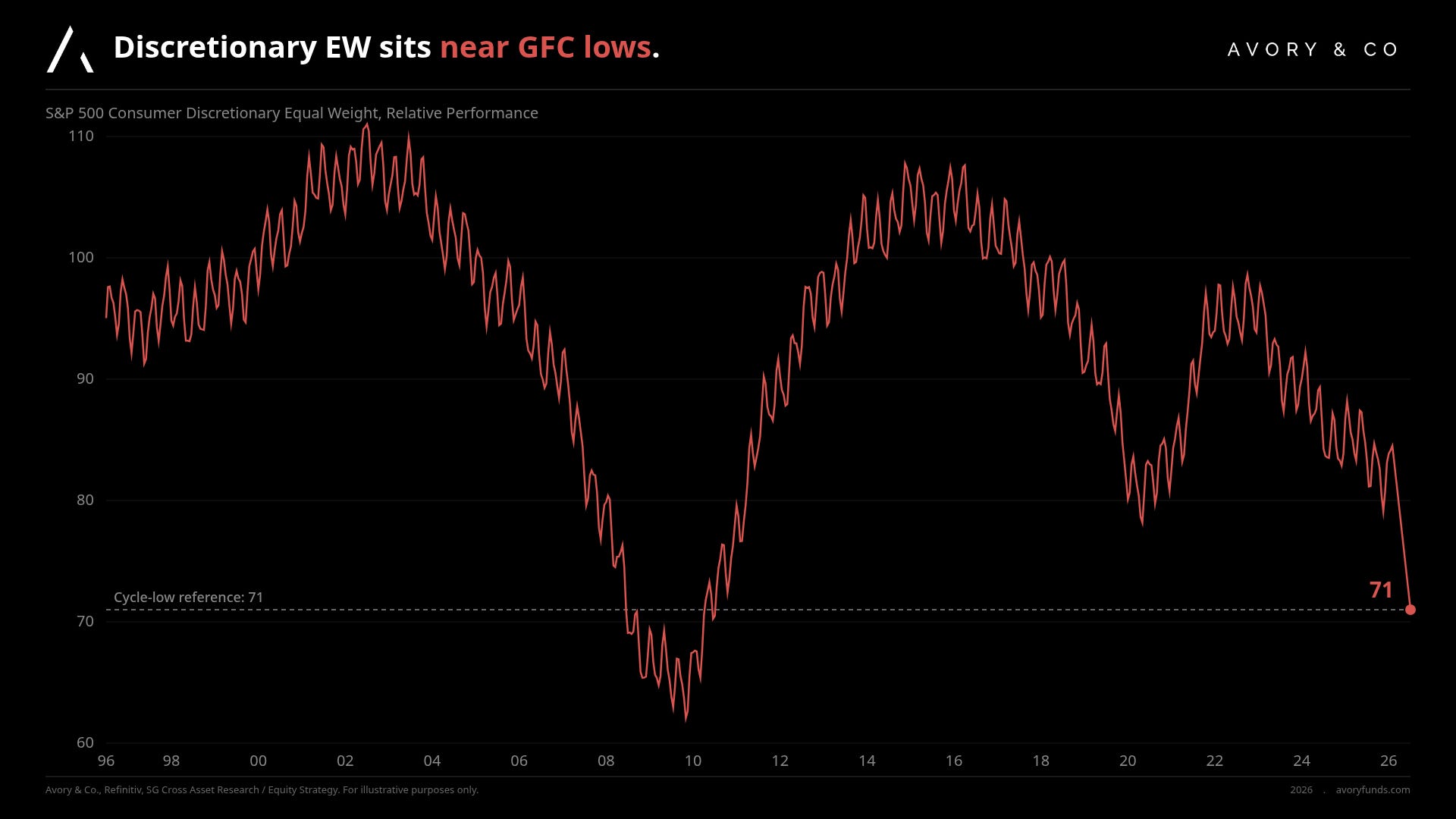

[7] Consumer Discretionary equal-weight is back at cycle lows.

This one is wild.

On a relative basis, discretionary equal-weight sits back near great financial crisis lows despite the economy doing good enough. This is further evidence of what we’ve been talking about for the last couple of years. The market has been pretty fearful of what’s happening in inflation and the economy, and yet inflation and the economy have gone counter to those negative views.

Our read has been fairly constructive. To us as long-term investors, we see opportunity here from a valuation perspective and a quality perspective, and we continue to be long certain pockets of it.

Since the ceasefire took place, discretionary started to levitate. While the ceasefire is somewhat in question, the magnitude of the implications look less impactful today, and we should start to see the broadening trade continue, including discretionary.

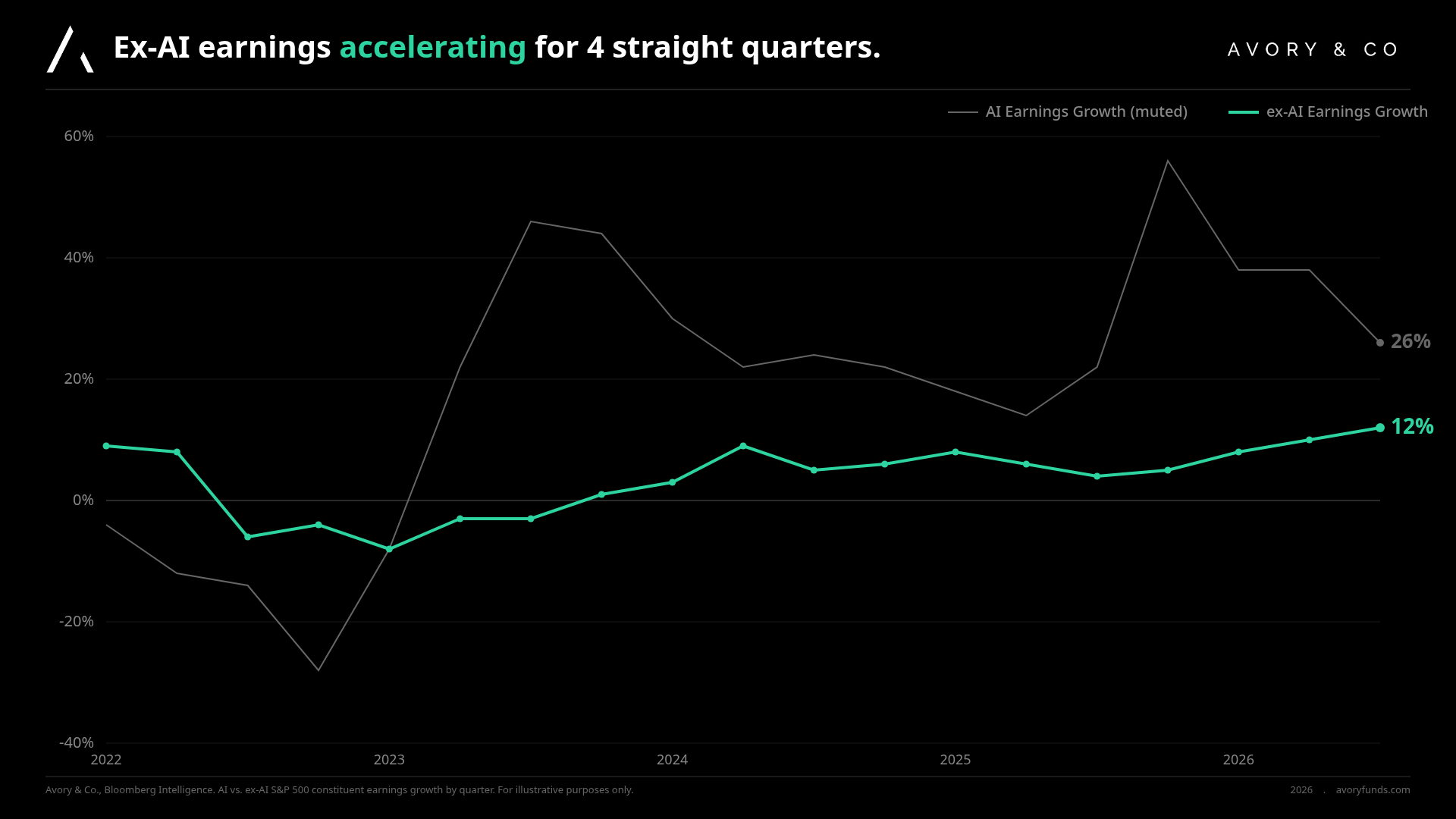

[8] Non-AI earnings are accelerating.

Why broaden? well.

AI earnings growth is still running well above the rest of the index, no argument there. But the story here is the other bar. Ex-AI earnings growth has been accelerating for four straight quarters and has flipped clearly positive. That underpins the broadening trade, and it’s probably a big part of why we’re seeing the transition. Doesn’t guarantee it, but the setup is in place. Same story, different week.

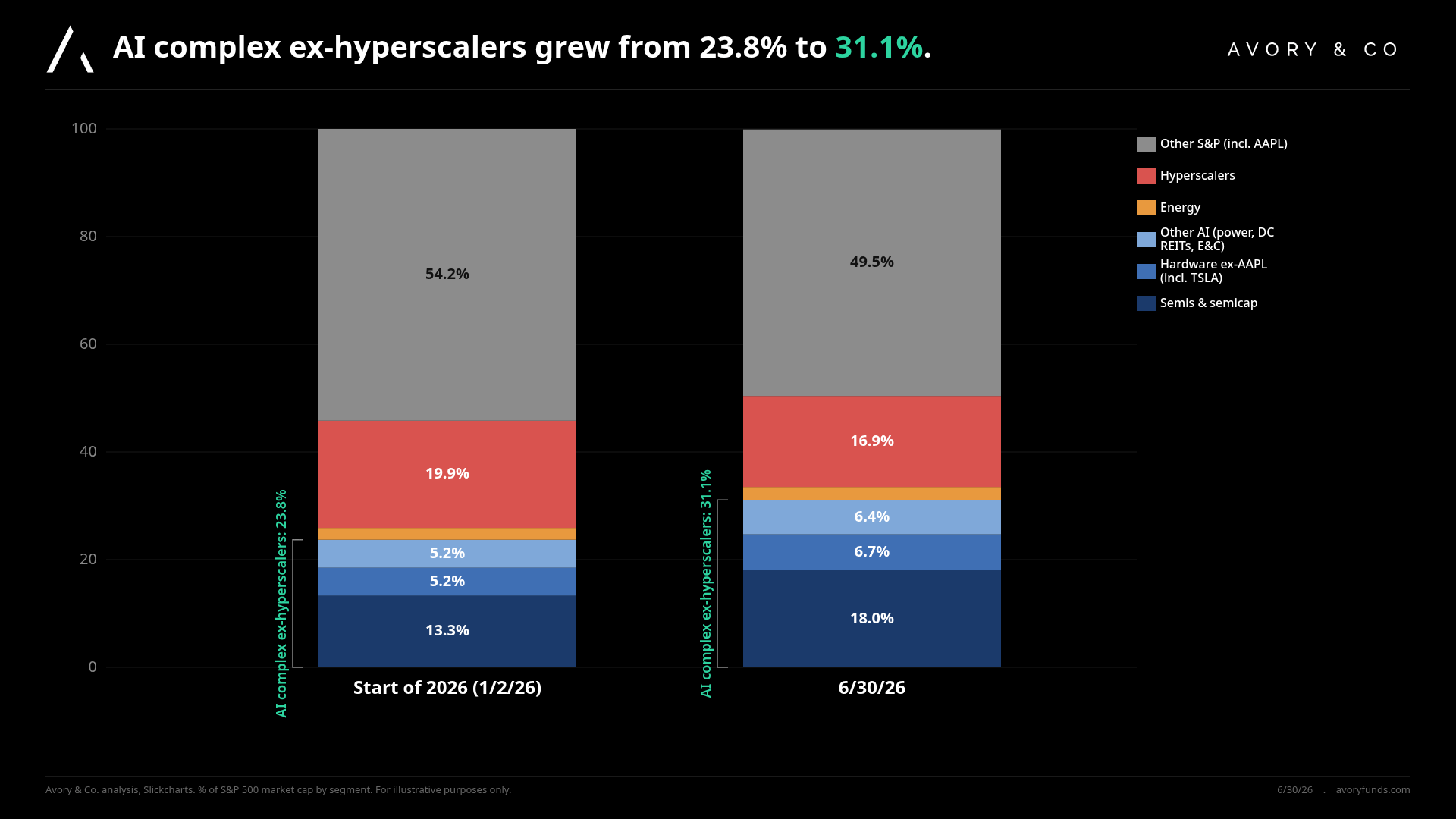

[9] The AI complex is now roughly a third of the S&P.

This one pairs directly with the last chart. From January 2 to June 30, the AI complex ex-hyperscalers grew from 23.8% to 31.1% of the S&P 500’s market cap. Semis and semicap alone went from 13.3% to 18.0%. Hyperscalers ticked slightly lower, from 19.9% to 16.9%. Other S&P, which includes Apple, dropped from 54.2% to 49.5%. So if non-AI earnings are accelerating, and AI dominates the index, then the question becomes: should you be considering the non-index? Or a little of both. That’s where our head is at.

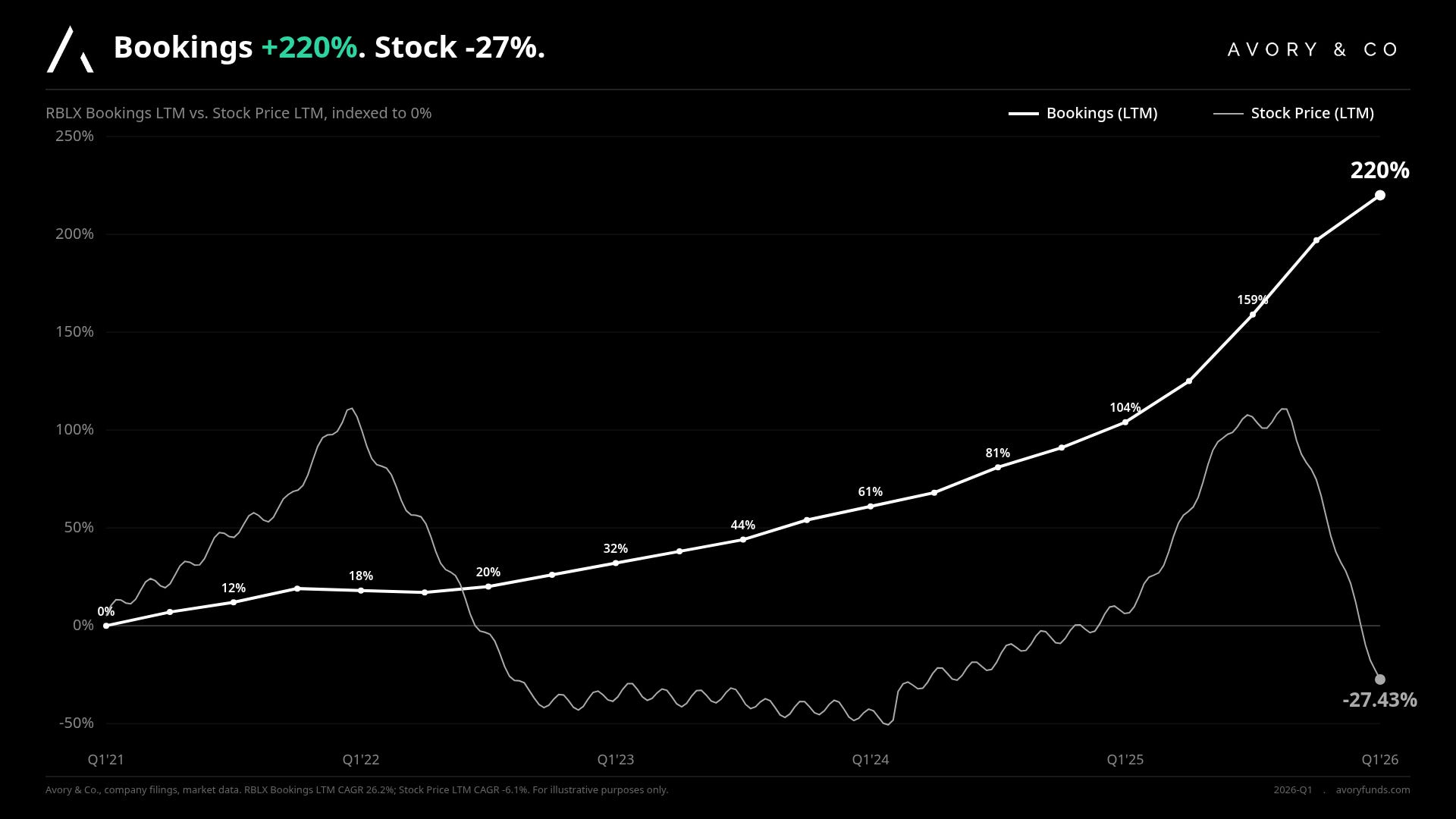

[10] Good example of dislocation.

Someone asked me the other day, “what does dislocation mean?” Here you go.

This is a really clean reflection of how you can have a detachment between a company’s fundamentals and its stock price.

Roblox bookings are up 220% since Q1 21, a 26.2% CAGR. Stock is -27% over the same window. Part of it is nuances specific to the Roblox story, but this is less about Roblox directly and more about the idea that over the last year you’ve had people questioning what AI is going to do to certain digital assets, and questioning what’s going to happen in the economy.

These things tend to resolve favorably if the fundamentals continue to persist in a constructive way.

There are a bunch of these divergences out there right now.

[11] From Signal 42… Oil surged 7.2% in a single day.

Oil moved 6% to 7% roughly Wednesday. Signal 42 pulled the history of 1-day moves of 7.2% or more going back to 1986, and typically when you get these type of large moves they mark transitions from one period to another.

We saw the rise in oil during the conflict, and now we’re simply seeing moves on the way down as people question what’s happening in the Middle East. Overall, if you look over the last 5 years, oil prices have pretty much stayed in this range. In theory, if you weren’t concerned about $70 or $80 oil 5 years ago, you shouldn’t be all that concerned today either.

Net Net

Rotation is showing up. Non-AI earnings are accelerating, real-time engagement data at Cash App and the prediction markets is running hot, corporate identity spend is validating the Okta and Clear thesis, and Consumer Discretionary is sitting at relative lows even as economic conditions have remained steady. That is opportunity. Meta is back in the model game. Roblox is one of many examples of fundamentals detaching from price. That tends to resolve favorably over time.

That’s all for this week!

About Avory & Co.

Investing Forward.

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn’t constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us:

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube: Channel

🎙️ Avory: Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.