13 Charts: Earnings season is back + What Buffett Said…

Netflix, banks, Autonomous battle, Venmo data and more...

Big Picture

💡 Earnings season kicked off this week and the market is doing exactly what we’ve been calling for.

Happy Friday! On a plane here so wrapping up some of the data. This week was packed with info. My view remains pretty simple. We’re constructive on what’s been taking place. The rotation we’ve been talking about is happening, driven by a healthier macro views and people becoming less concerned about the Middle East. Oil isn’t responding as aggressively as it was. That can change, but it doesn’t change our view that the economy can withstand it either way.

Also if you look around, there have been a large swath of companies treading water for 6, 12, 18, even 24 months while continuing to grow revenues and bottom lines. That is opportunity. The banks reported this week and delivered clean prints. Always look at banks to give you a sense of economic activity. For the banks, net interest income and margins were positive across the board, deposit and lending growth were constructive, and the messaging on the economy and consumer was uniformly healthy. That is good and coincides with our new bank sentiment reading. See below.

A few other things caught our eye this week. The autonomous space is getting interesting. Amazon’s Zoox is gaining, literally have not heard anyone put Zoox in the same category as Waymo or Tesla, but I think they should start, see the data, we are. Venmo as an asset remains interesting, and ironically PayPal was reportedly bid for by Stripe, Block and Advent. That is a big deal and I suspect the offer goes higher after speaking around, but something to watch as it relates to competition for other fintechs. Credit card data below shows the consumer is fine, and the Venmo engagement data speaks to why the asset remains attractive.

Lots to share, let’s get into it.

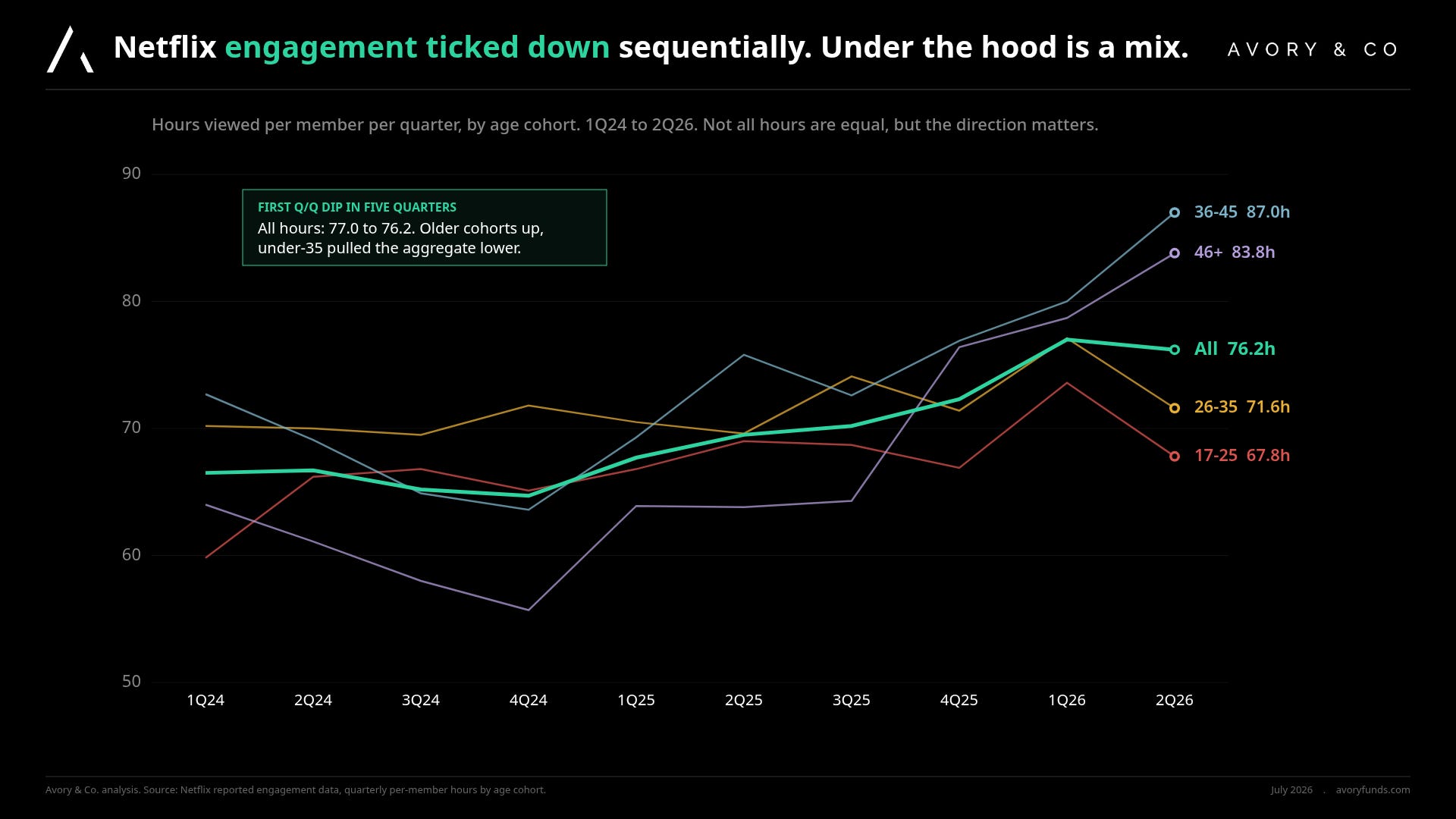

[1] Netflix engagement data down sequentially. Data we tracked flagged this ahead of time.

Netflix reported last night and first it is great to have earnings season back. Love it.

What we saw was generally healthy top line and bottom line. However, viewing hours per member fell sequentially for the first time in five quarters. On the earnings call Netflix’s answer was a constructive counter, not every hour is the same. Live shows and ad-supported content pull in more ad dollars per hour even if the time spent is lower, different from the traditional binge format of old.

We have been looking at Netflix for a while here as it is down 50% from highs, but Apptopia data was showing time spent per DAU falling Q/Q. So again great way to manage fundamental risk. We will be looking for a rebound, and Netflix may get interesting…

Under the hood, older cohorts actually moved higher, 36-45 hit 87 hours and 46+ hit 84 hours. The under-35 cohorts pulled the aggregate lower. Could that be social + YouTube? Not a large concern until it is, but again likely why the stock is down ~50% from highs.

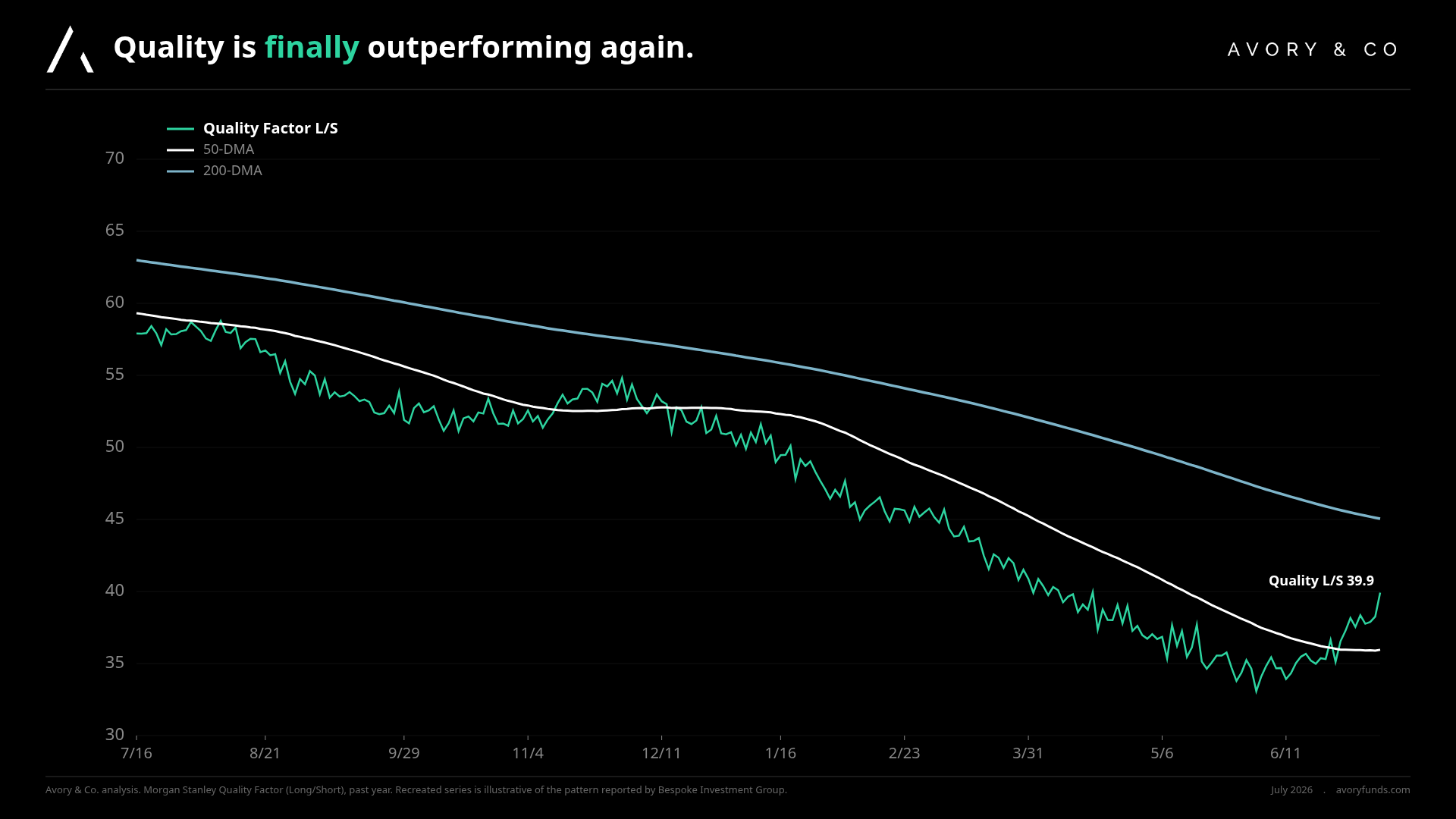

[2] Quality Factor is doing what it’s supposed to do.

The Quality Factor long/short has been on a run, and this is the setup we’ve been positioned for. Not for a trade, but for an investment in specific names that have been “placed” in that factor.

Rotation into quality is happening because the macro is healthier and has stayed that way. Also feels like middle east risk premiums are compressing, which is a positive, and rates fell over the last week or so on lower CPI + PPI falling

So again a thesis we’ve been explicit about. When Quality outperforms it usually says the market is rewarding earnings power, not just multiple expansion for high flying momentum names, and that lines up cleanly with what the banks showed also.

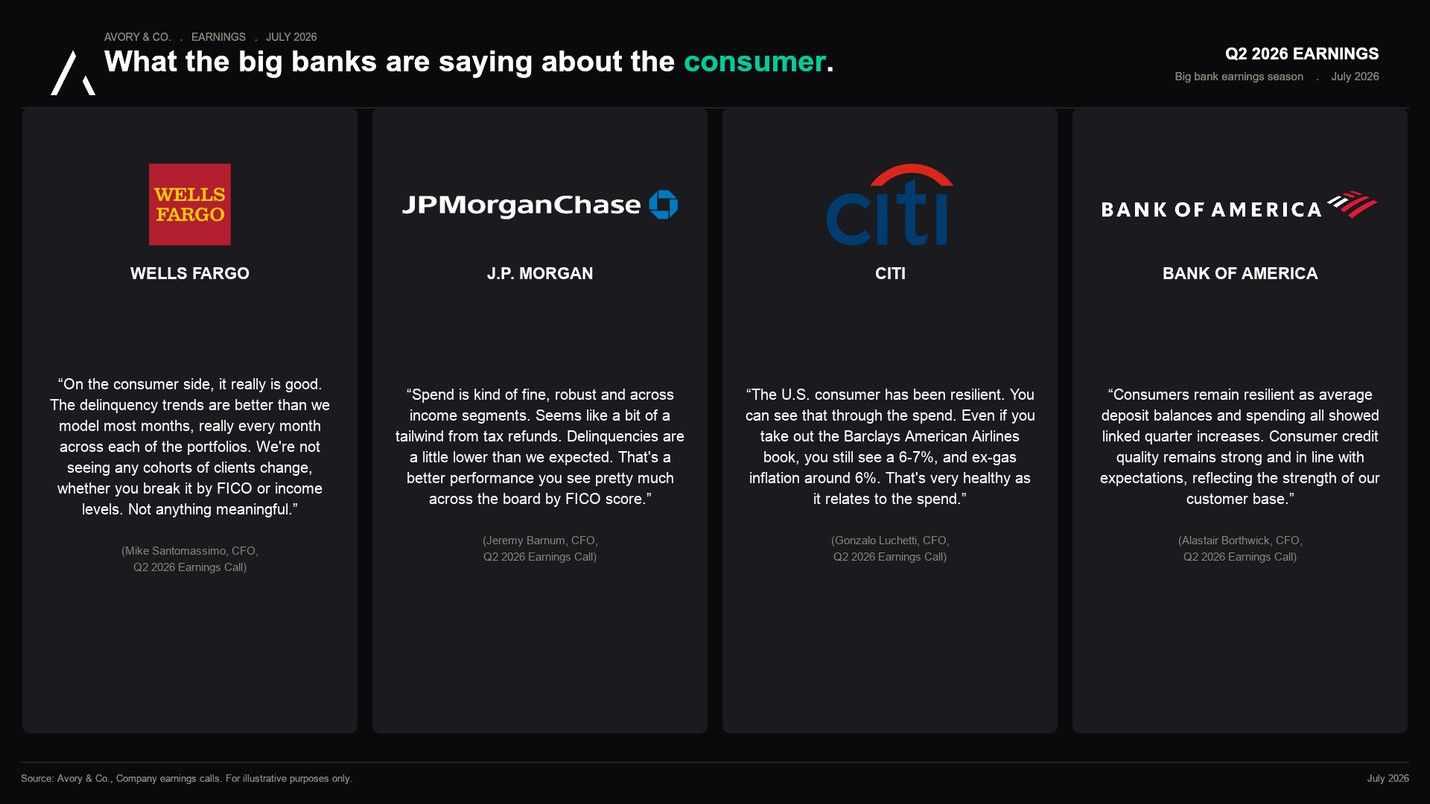

[3] Banks came in clean across the board.

Consumer comments

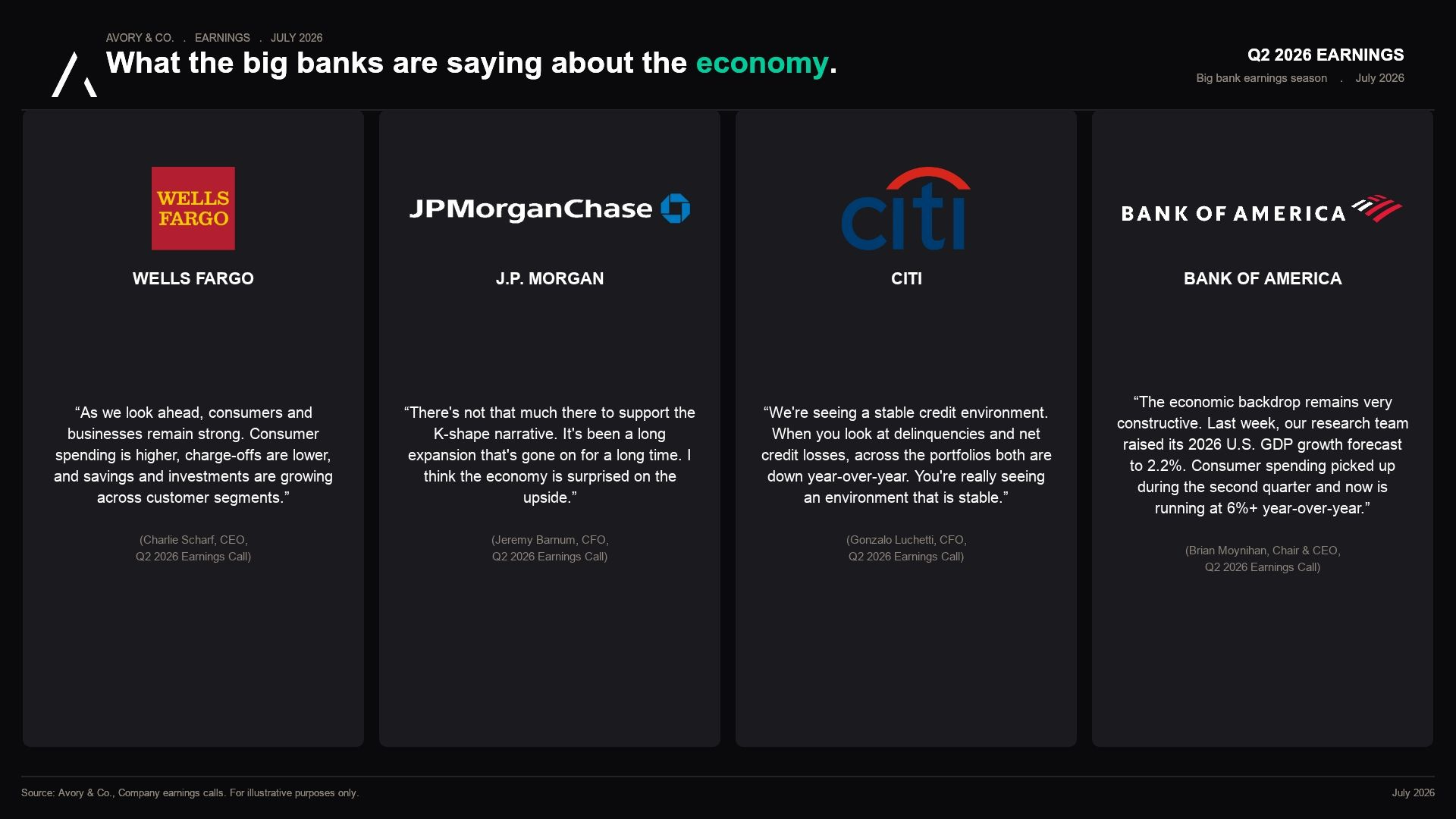

Economy Comments

Let’s dig into that for a second. The big banks reported this week and the message was clear. Net interest income and margins were positive across the majority of them. Deposit growth and lending growth were both healthy. Each has their own nuances so we won’t get lost in the weeds.

The cleanest take is that the banks that control the majority of deposits and loans in the U.S. all delivered clean messaging on the economy and the consumer. All of them said the same thing. Hard to find any negative tilts.

[4] Our bank sentiment reading keeps perking up.

We now track CEO/CFO sentiment reading across the big banks. Every quarter we pull their earnings commentary and score whether their views on the consumer and the economy skewed positive or negative relative to the prior print.

This quarter’s reading continues to perk up.

Both the Economy and Consumer heatmaps are green across the board, and the quotes panels underneath show exactly why. Also read the main quotes, very constructive read as the messaging is remarkably consistent across the biggest banks in the country. In aggregate, many things are healthy, spending is fine, credit is holding, and there’s no sign of imminent stress in the underlying data. Good news.

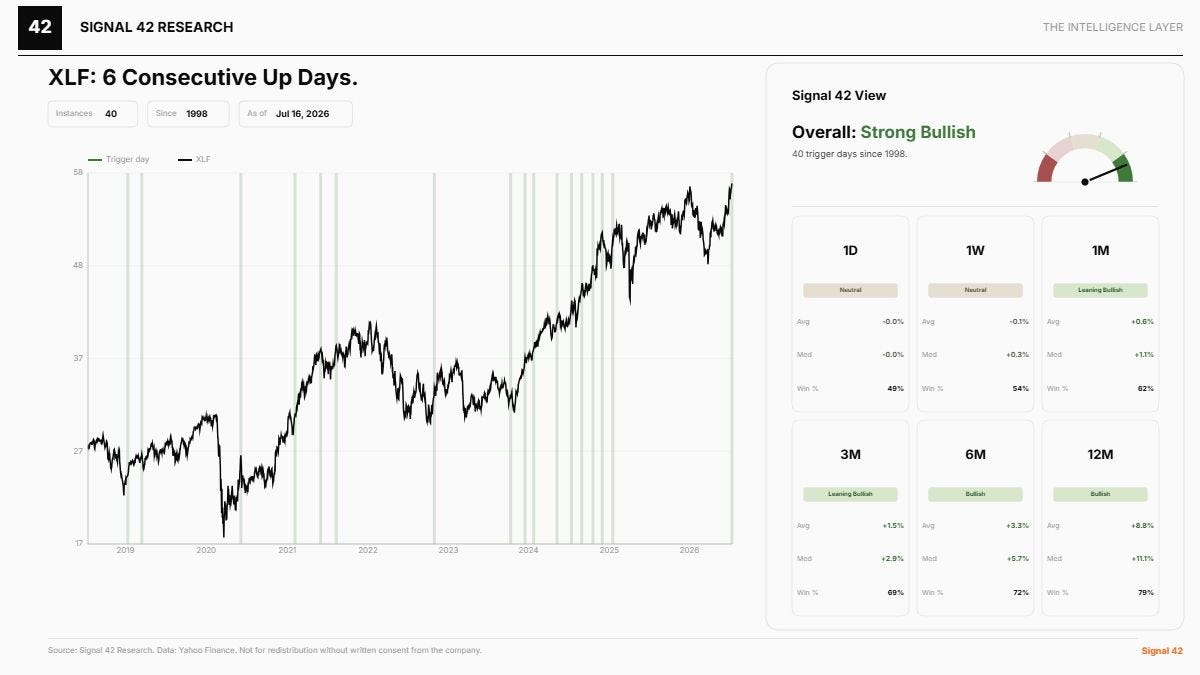

[5 ] Financial Index, XLF just posted six consecutive up days.

On top of that, Signal 42 flagged XLF for six consecutive up days into 7/16. Financials leading the markets is never a bad signal. We have only seen this 3 times over the last 20 years where financials were up 6 days in a row while consumer discretionary was up 3 days in a row, and the market 12 months later has been up 100% of the time with an average return of +20%.

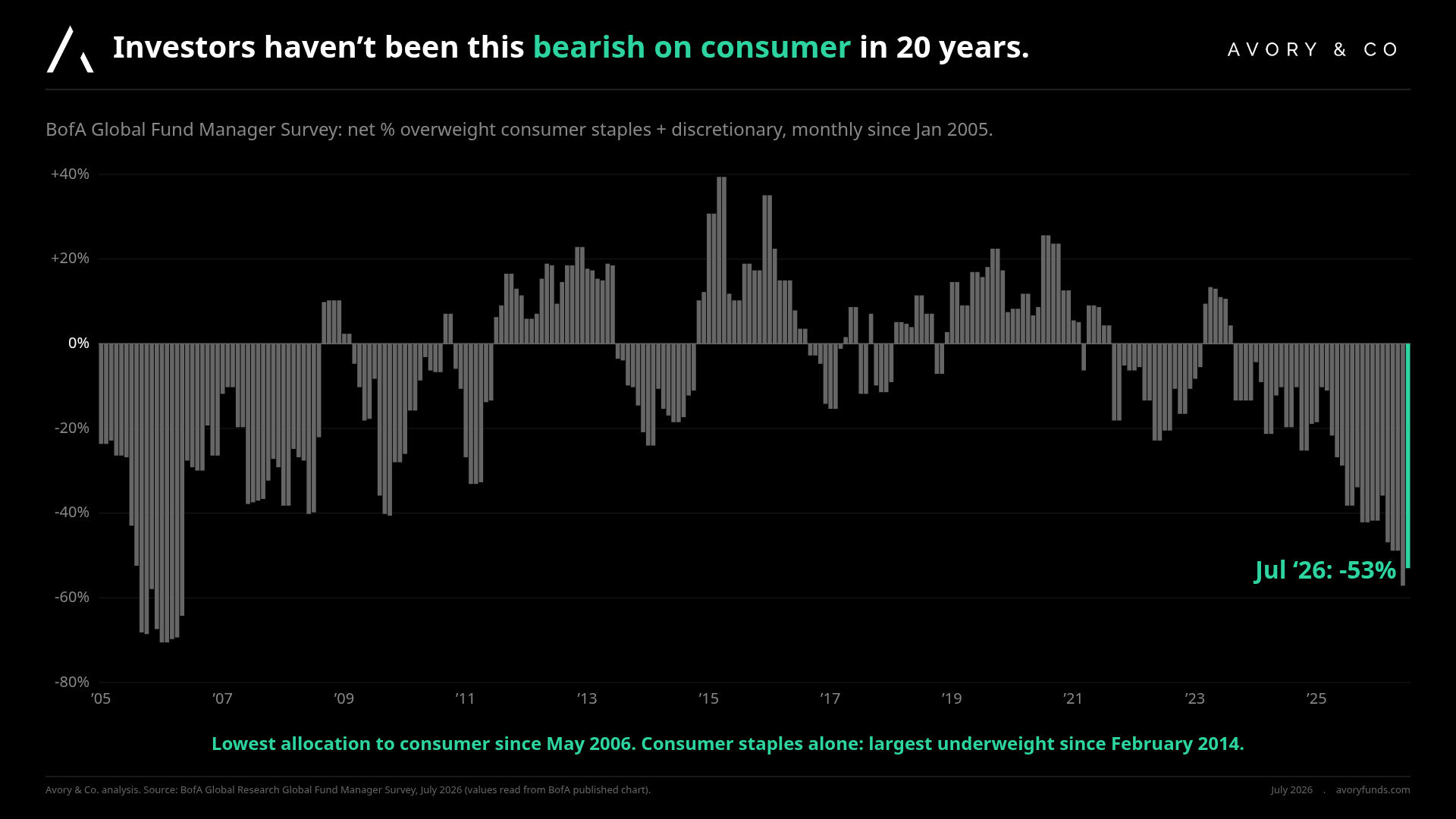

[6] Investors haven’t been this bearish on consumer in 20 years.

Then looking at the Fund Manager Survey that shows net allocation to consumer stocks (staples + discretionary) is at the lowest level since May 2006. Investors haven’t been this under-exposed to consumer names in 20 years. People are getting less concerned about the economy and rate hikes, and more concerned about AI. That leaves a real contrarian setup here. But again, this echoes our ongoing view that this area is ripe for activity.

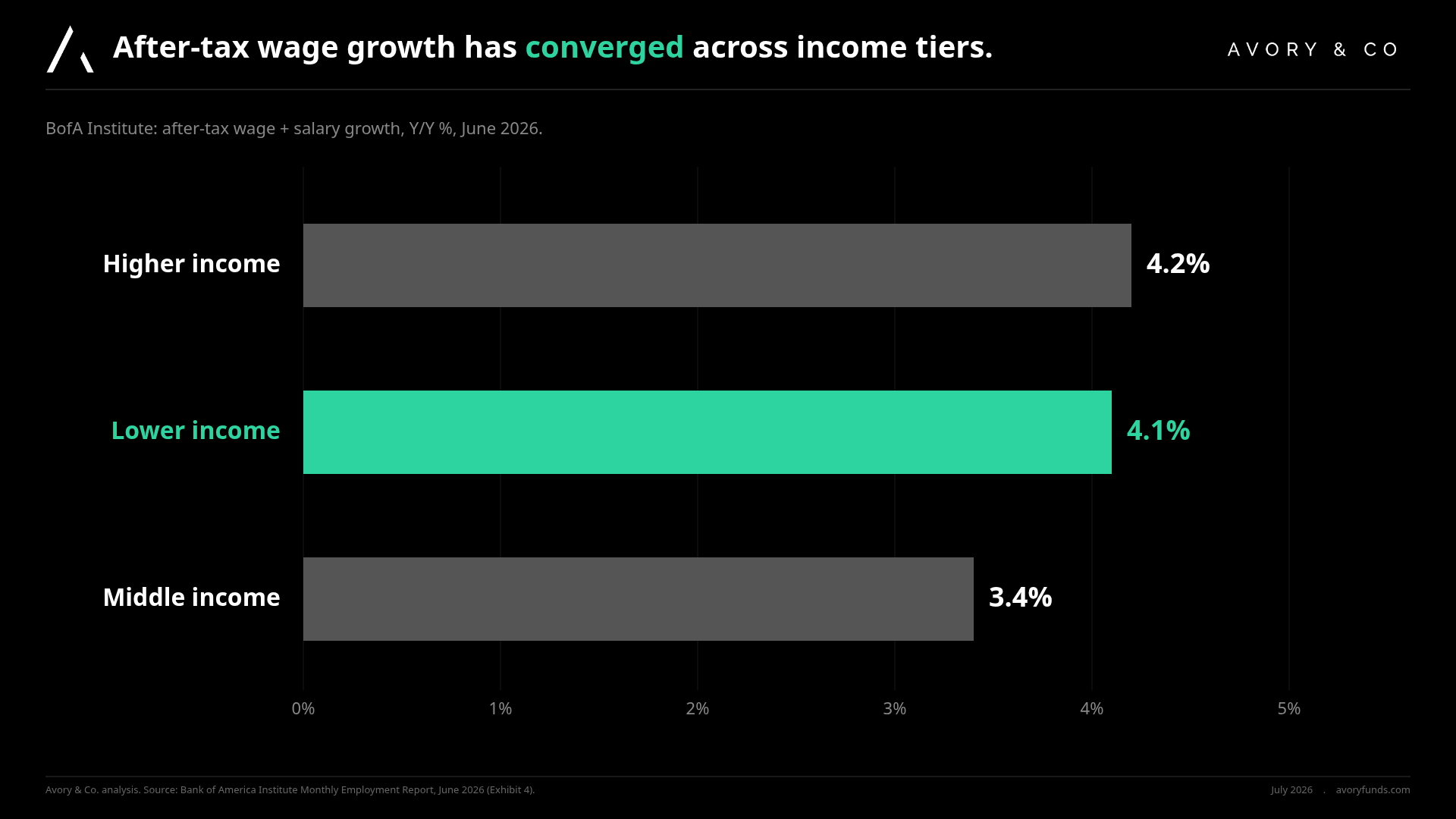

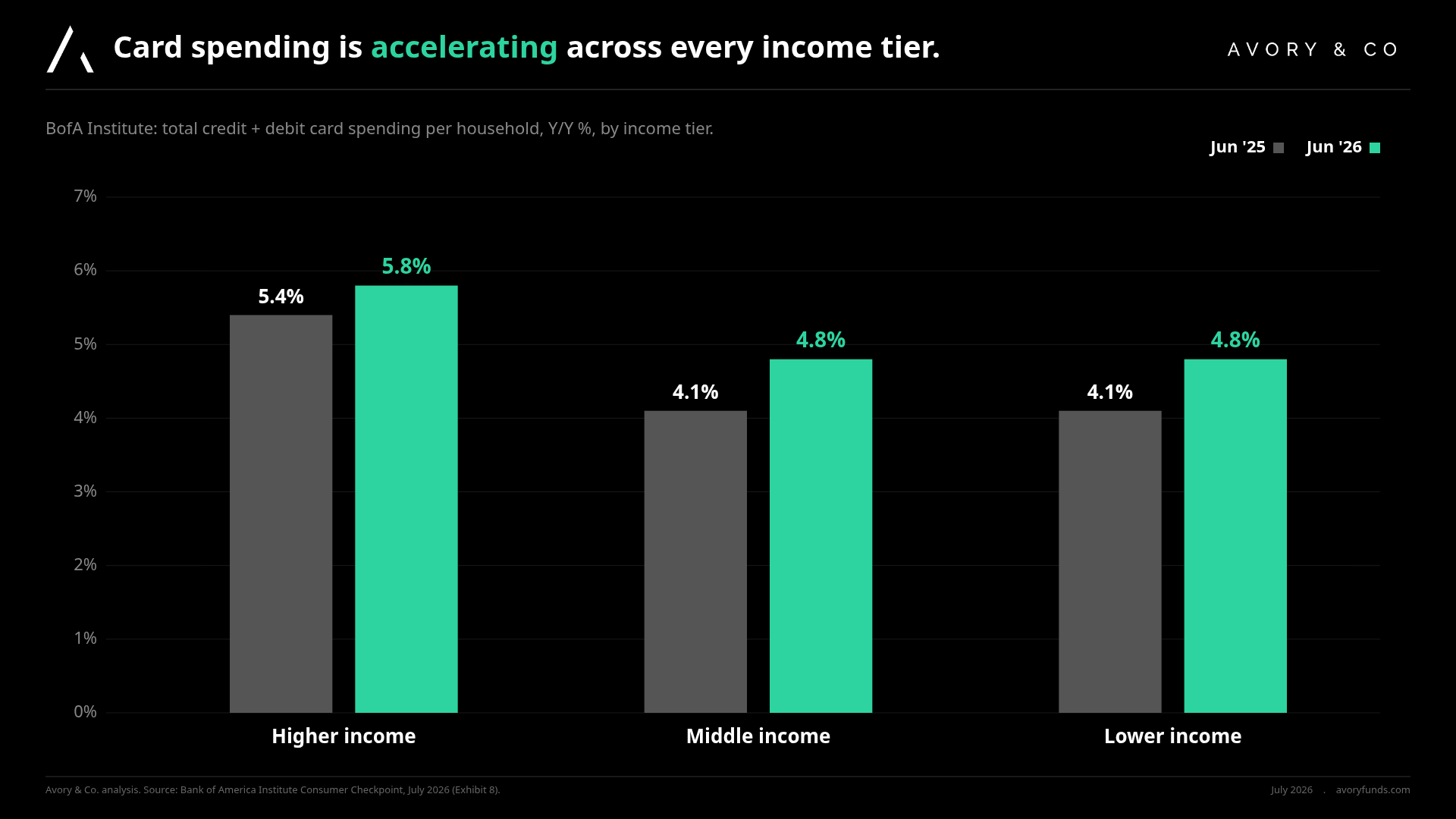

[7] Real consumer data says the “consumer is cracking” story is wrong.

We have two charts here that are essentially saying the same thing, but differently. BofA’s card spending data by income group shows spending accelerating across every tier.

Higher income +5.8%

Middle +4.8%

Lower +4.8% Y/Y as of Jun ‘26.

Same pace, all three moving together. Then their after-tax wage growth chart shows the same convergence. Higher +4.2%, Lower +4.2%, Middle +3.5%.

When you tax-adjust, wage growth across income tiers is essentially running at the same rate. Real wages are positive across the board despite what others suggest, we shared in prior pieces. This is the data the underweight consumer positioning is missing.

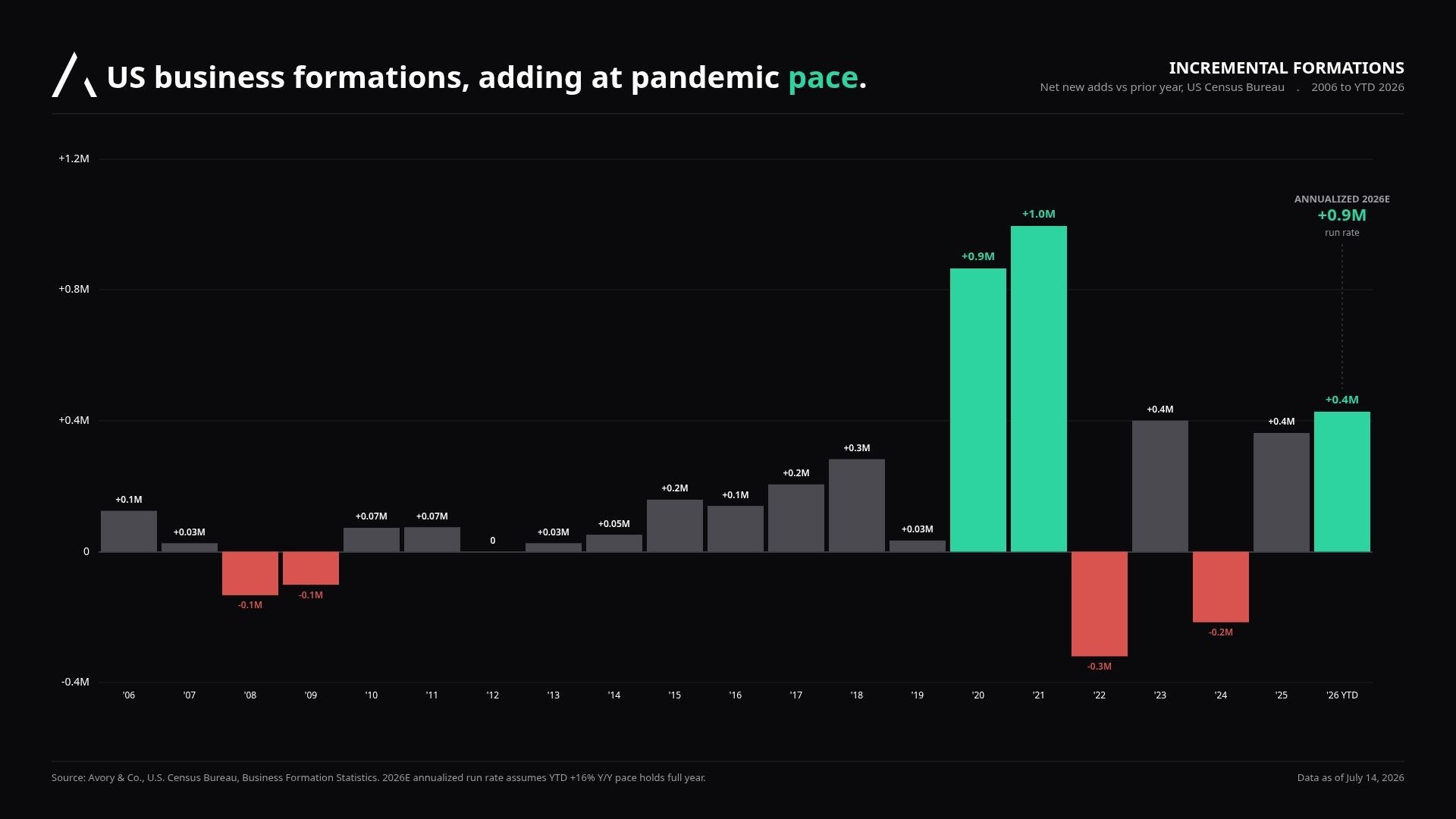

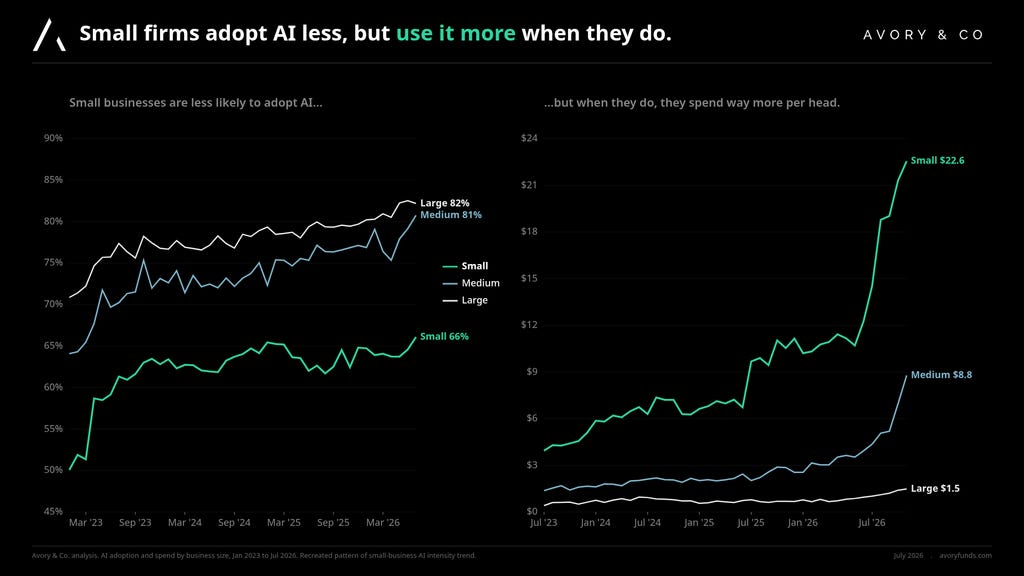

[8] Business formations and AI adoption both say the underlying economy is healthy.

Business formations continue to run at elevated levels. We have pointed to this for a while now. That’s a leading indicator of economic activity. Underneath that, AI adoption is broadening out.

Small firms adopt AI at lower rates than large firms, but when they do adopt they use it more intensively. AI is a net positive for the economy in the way it’s diffusing, and it shows up in the productivity of businesses that are actually deploying it.

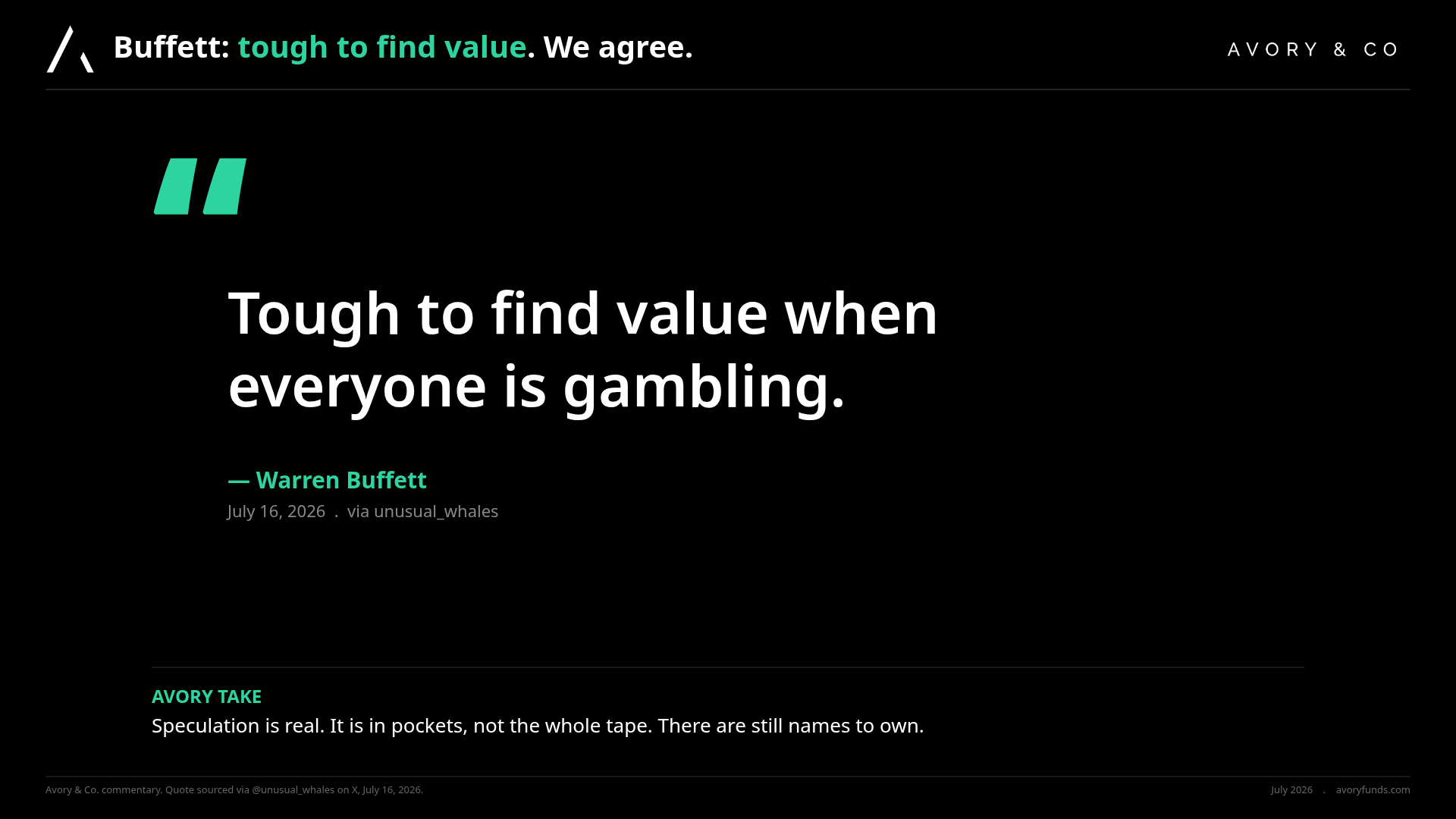

[9] Even Buffett noticed the speculation. We agree.

Warren Buffett said this week that it’s tough to find value when everyone is gambling. We agree. There is speculation in the markets right now, and it’s real. But it’s in pockets, not the whole market. Really around AI, Space, Chips etc. There are still names to own in those areas where the fundamentals are compounding and the multiple hasn’t gotten silly. That’s where our attention sits. Speculation somewhere doesn’t mean overvaluation everywhere. So good to separate those two views clearly.

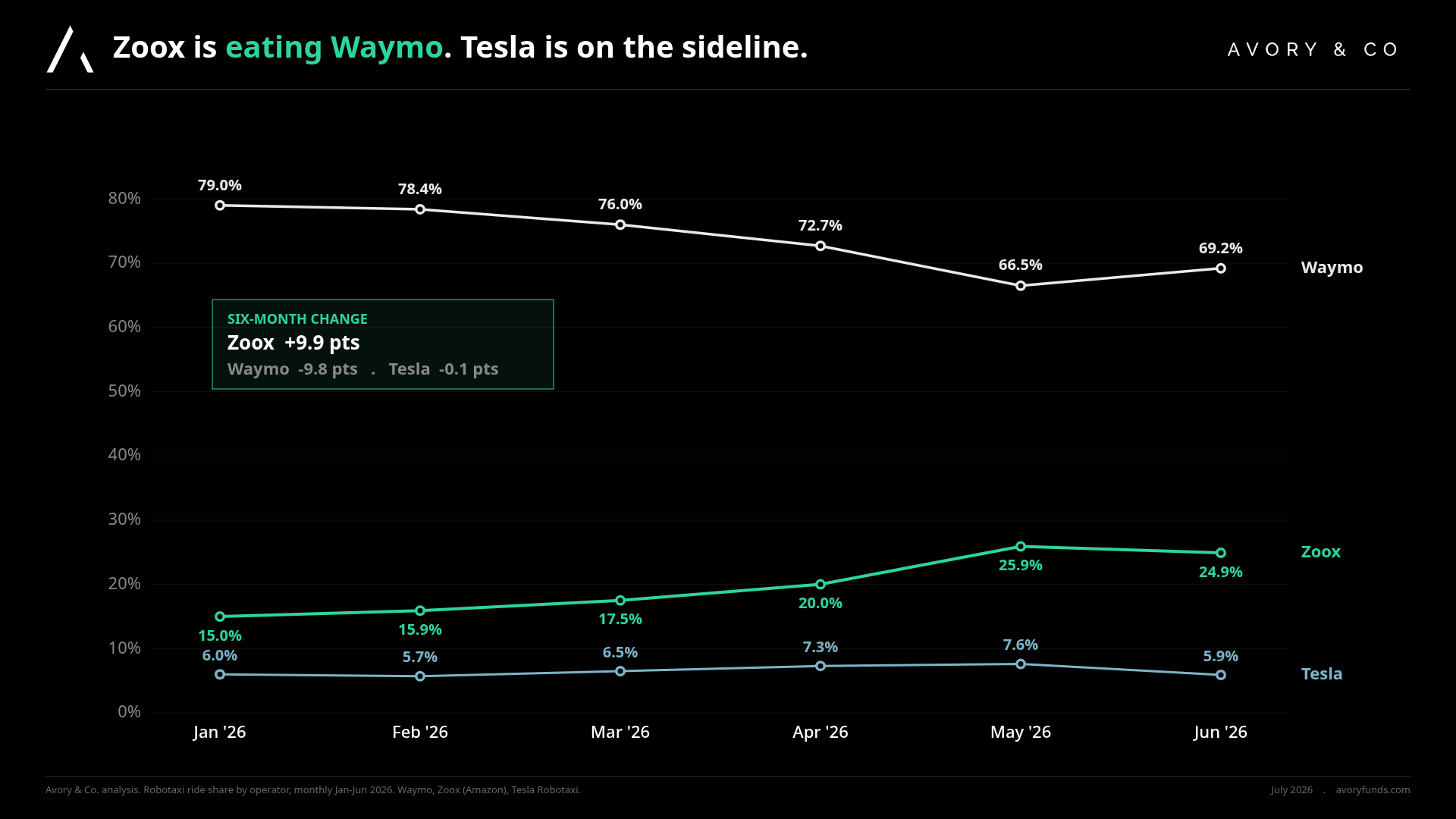

[10] Robotaxi share is shifting fast.

Robotaxi is one of the pockets where actual operator progress is showing up in the data. Apptopia data shows that Zoox is taking share from Waymo faster than most people appreciate.

Pay attention…

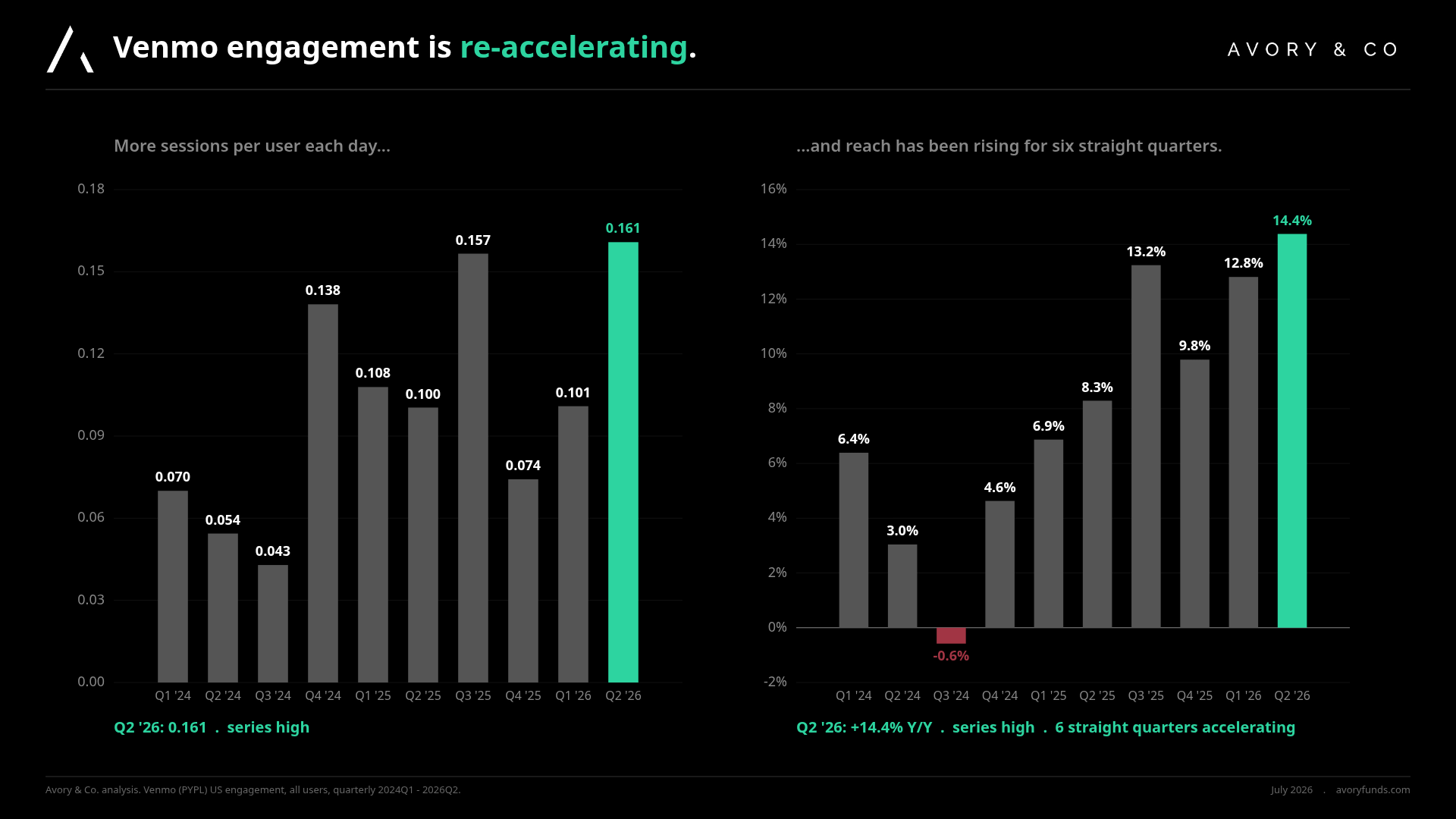

[11] Venmo engagement is re-accelerating.

PayPal, which owns Venmo, was offered this week to be taken private. Suitors are a consortium of Stripe, Block and Advent. Now why? One part is their Braintree processing business, another part is their PayPal branded business. Lastly is Venmo, their consumer engagement layer.

Now how is Venmo doing?

Apptopia data shows that Venmo’s engagement metrics are re-accelerating after a stretch of flat reads.

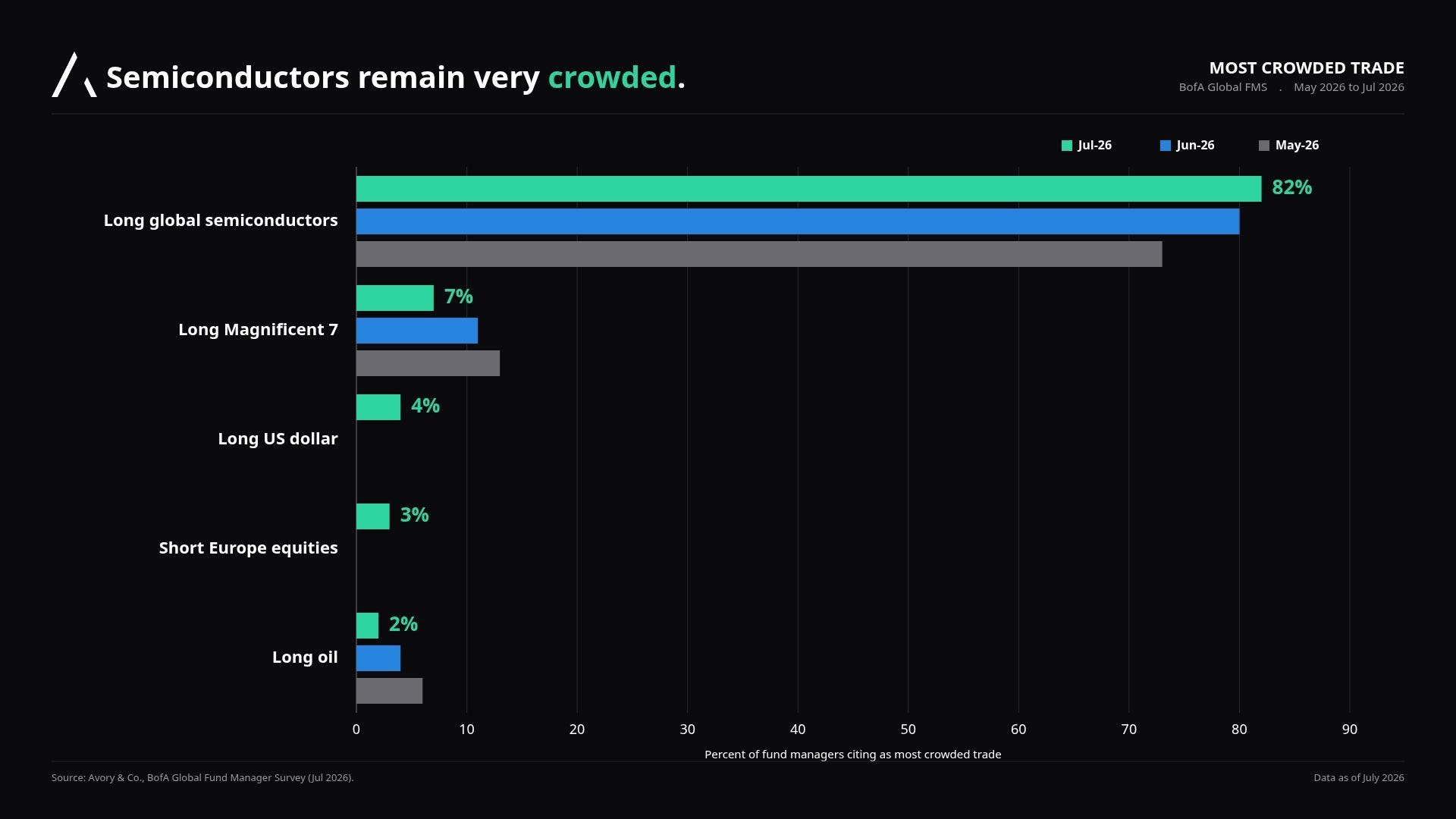

[12] Semis are the crowded pocket. Etched shows competition is coming.

More data on investment positioning. Long Mag 7 and AI semis came in as the most crowded trade globally. Probably why, when there is some selling pressure, we see exaggerated moves. But there are some things to think about within the AI trade. A company like Etched just showed their Frontier Inference Clusters, purpose-built inference silicon designed to run transformers faster and cheaper than general-purpose GPUs. This is what we’ve been saying about the inference layer. As models stabilize, margins show up in the infra layer. Companies will look to either create their own silicon to sell, or use custom silicon. This does not mean that it kills companies like Nvidia, but it does re-shape the margin structure over time. Something to keep tabs on.

Net Net

So earnings season is back and the first reads are constructive. Banks are healthy, the consumer is spending, wages are positive after tax, and the economy underneath continues to form new businesses and adopt AI. Positioning in consumer is washed out at 20-year lows, which is exactly the setup we’d want to see for a contrarian move. Speculation is happening in certain pockets, we agree with Buffett there, but the broader market is doing what we’ve been calling for. Rotation into quality, financials leading, and the companies that have been treading water while growing are starting to work. That’s the story of this week.

That’s all for this week!

About Avory & Co.

Investing Forward.

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn’t constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us:

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube: Channel

🎙️ Avory: Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.