9 Charts: Here come the IPOs.

Big Picture

💡 Here come the IPOs. History says be patient.

Anthropic just filed for IPO, and this is just after raising a series H (moving down the alphabet). A $65B round at a $965B valuation, OpenAI is on deck, and the AI IPO calendar is loading up fast as they see the window.

Side note, our strategy when you do look through exposure to OpenAi + Anthropic, its roughly 5-10% weight (depends on dilution at IPO) into those two combined.

Overall we are constructive on the cycle beyond AI, but the data from the last IPO cycle is hard to ignore, specifically for the companies that IPO.

Now Berkshire just deployed roughly $20B into acquiring housing company Taylor Morrison, and putting $10B into Google. So hard to get too worried when one of the more prudent allocators is putting significant amounts of capital to work at this time. Keep in mind they have underperformed by about 30% over the last 12-18 months similar to other GARPy investors.

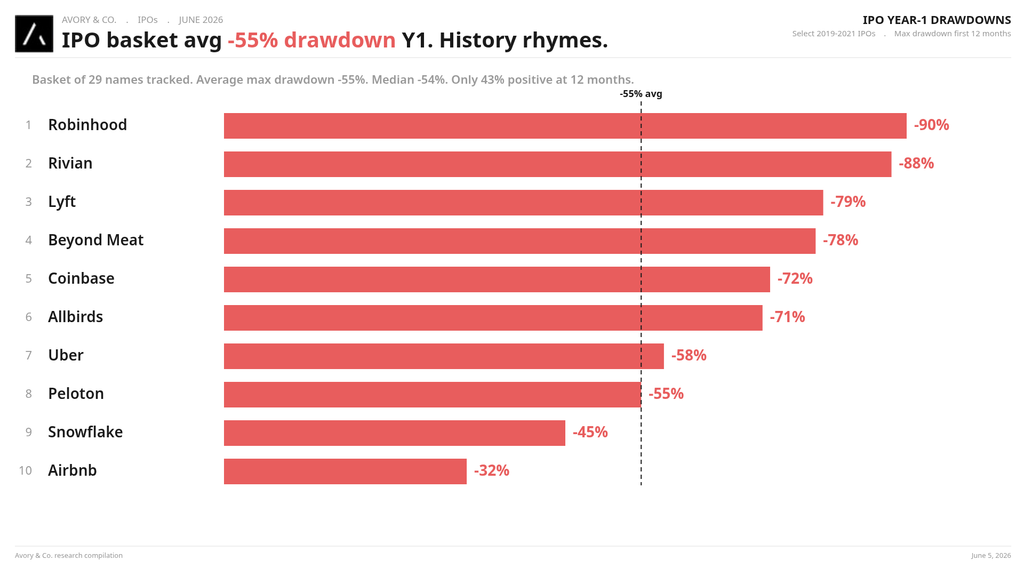

Back to IPOs, we saw a chart floating around showing 29 IPOs from the 2019-2021, what’s crazy is that wave averaged a -55% max drawdown in Year 1. Median was -54%. Only 43% of them were positive at the 12-month mark. So the AI names eventually coming public will need to be priced into a market that already remembers that math. Maybe it’s a known known so market does opposite. But these will have $1T + starting points.

Now the macro underlying data remain stable. We are seeing software become less binary. Late last week IGV, the software index printed the most overbought reading we've seen since early in the year and historically that setup has been bullish, not bearish.

Also covered this week is how Meta is taking share inside the genAI ad economy at a pace nobody else can match. ChatGPT hit 1B MAUs in three years which is the fastest any consumer app has ever scaled. The Revelio labor tracker bounced for the first time in six months. we got a lot to go over.

[1] IPO basket averaged a -55% drawdown in Year 1. History rhymes.

29 names tracked from the 2019-2021 IPO window.

Robinhood was -90% in Year 1. Rivian -88%. Lyft -79%. Even names that recovered (Airbnb, Snowflake) carved out -32% and -45% intra-year before they did.

Average max drawdown -55%, median -54%, and only 43% of the basket was positive at 12 months.

So when Anthropic files at a $1T or more valuation and OpenAI lines up behind them, you can be constructive on the underlying businesses and still believe the printed prices need time.

We've also got Alphabet running an $80B equity raise around this same window, which says a lot about how much capital this AI cycle wants.

[2] IGV 99th percentile overbought. Historically that's bullish.

IGV +5.3% last Friday was great to see. First close above the 200-DMA since January 7. RSI above 80, more than 3 standard deviations above the 50-DMA. On the surface that reads too far too fast. Likely true but the historical setup after IGV closes above the 200-DMA with RSI >80 following a multi-month drawdown averages a +23.5% forward 12-month return versus +10% all-period baseline.

Software is one of those moves where the overbought reading after a long drawdown has been the entry, not the exit.

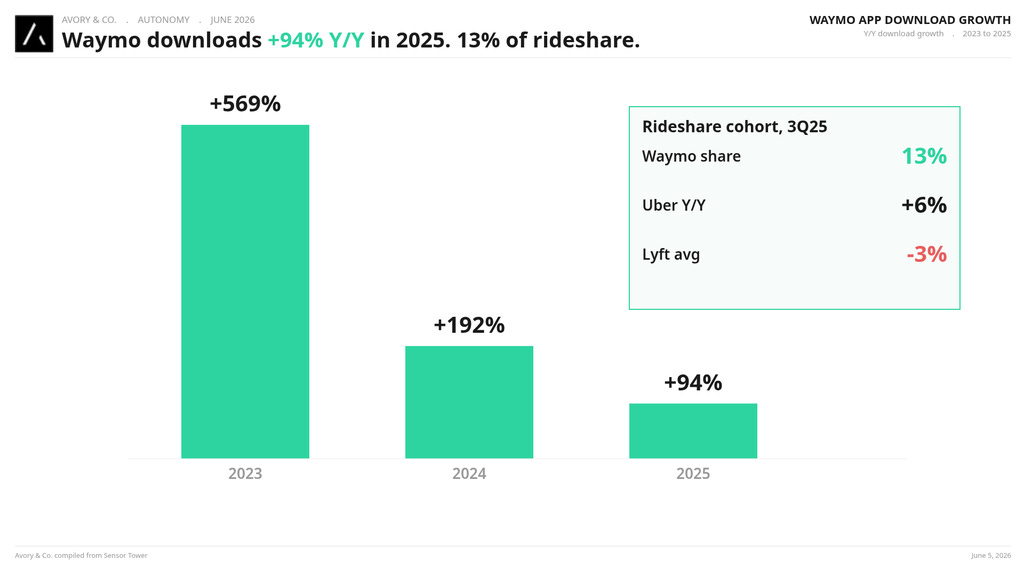

[3] Waymo downloads +94% Y/Y in 2025. 13% of the rideshare cohort.

We continue to track autonomous vehicles as it’s the future.

Waymo download growth was +569% in 2023, +192% in 2024, and +94% Y/Y in 2025.

The base is bigger now so the rate moderates, but the absolute share is interesting. 13% of the rideshare cohort downloaded Waymo in 3Q25. Uber downloads +6% Y/Y, Lyft averaged -3%. Feels like autonomy went from a science project to a measurable slice of the rideshare cohort in 24 months. Worth tracking against the autonomy thesis we've been carrying.

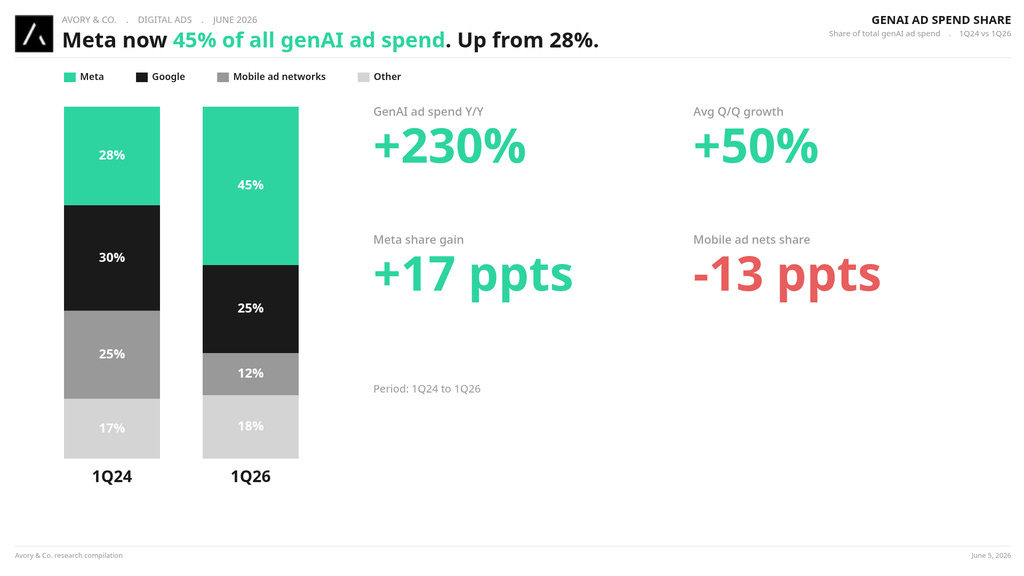

[4] Meta now 45% of all genAI ad spend. Up from 28%.

Meta's share of genAI ad spend went from 28% in 1Q24 to 45% in 1Q26. Google held roughly flat at 25%. Mobile ad networks lost 13 percentage points. Total genAI ad spend +230% Y/Y, averaging +50% Q/Q across the eight-quarter window.

We're seeing the same thing in the traditional advertiser data: CAC compression on Meta, ROAS expansion on Meta, share consolidation on Meta.

The franchise quality on a platform like Meta is showing up in the AI economy in real time. We remain confident that Meta is big AI winner.

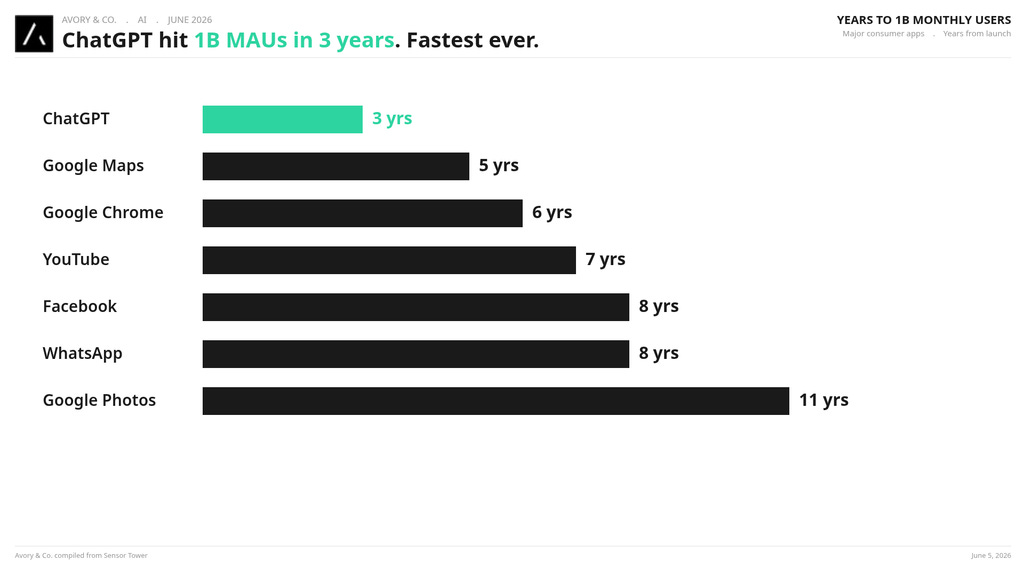

[5] ChatGPT hit 1B MAUs in three years. Fastest ever.

Different times as things get faster but Google Maps took 5 years. Chrome took 6. YouTube took 7. Facebook and WhatsApp took 8. Google Photos took 11.

ChatGPT did it in 3.

And ChatGPT now has more users than Gemini, Doubao, DeepSeek, Meta AI, Claude, Grok, Perplexity, and Copilot combined. That's a crazy adoption curve for the “number 2” in AI right now.

Whatever you think the right narrative is around AI, the user count is growing.

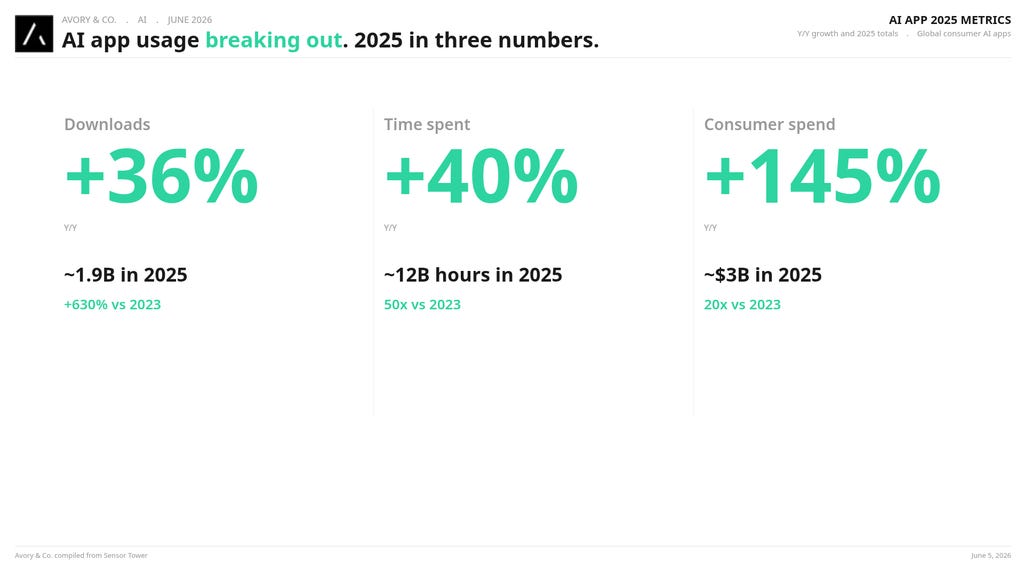

[6] AI app downloads +36% Y/Y, time +40% Y/Y, spend +145% Y/Y in 2025.

The 3 numbers tell a pretty big story. ~1.9B downloads in 2025, ~12B hours spent, ~$3B in consumer spend. Vs 2023 the multiples are +630%, 50x, and 20x respectively.

Spend is key tho. Consumers will pay for AI apps and they're doing it at a rate nothing in consumer tech has ever matched in a 24-month stretch.

We have also shared in the past that retention in AI is pretty bad early on, but cohorts as they mature get better.

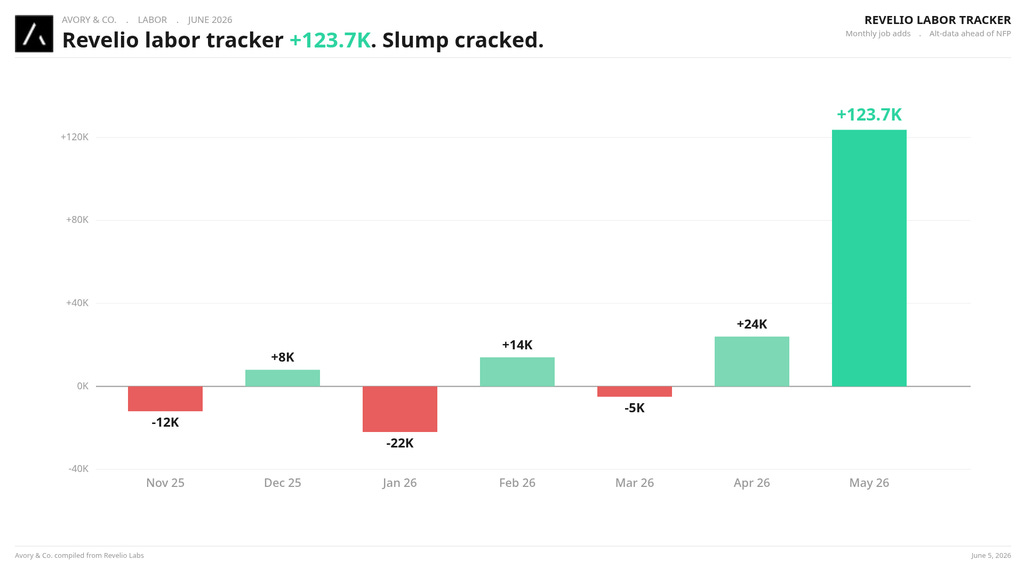

[7] Labor tracker +123.7K in May. First clean bounce in six months.

Revelio is the alt-data labor tracker we follow ahead of NFP. It combines private payroll signals with ADP-style inputs. The last six months printed flat-to-negative reads (-12K, +8K, -22K, +14K, -5K, +24K) which was part of why people were worried about the labor cycle cracking. May printed +123.7K. NFP itself drops / dropped today depending on when you read this. (Actually just dropped before I press post, and 172k jobs for NFP, and private payrolls 120k right where our data said)

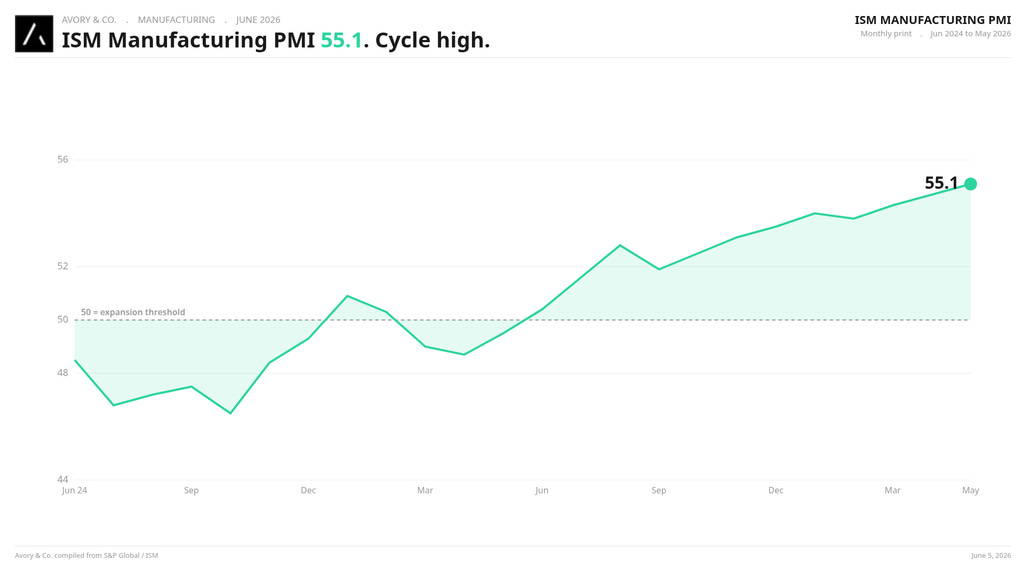

[8] ISM Manufacturing PMI 55.1. Cycle high.

PMI revised from a 55.3 flash to 55.1 final but still the cycle high. Two-year arc went from sub-50 contraction through last year to a clean expansion regime now.

We've been tracking this against the soft-landing thesis and the manufacturing side keeps confirming it.

Growth is holding up where you'd expect to see weakness first if things were getting worse.

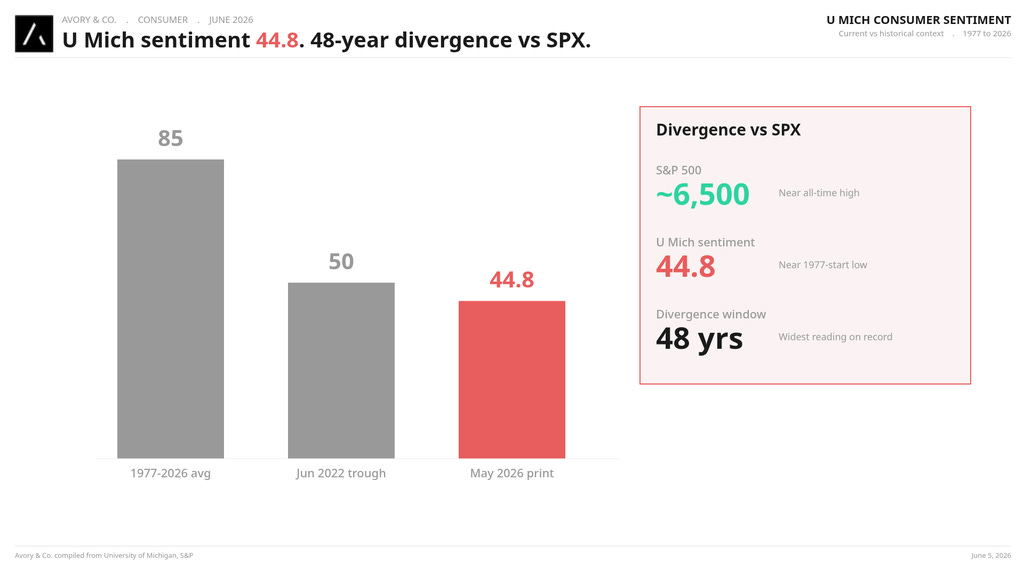

[9] U Mich consumer sentiment 44.8. 48-year divergence vs SPX.

All detail is like to share. SPX near all-time highs. U Mich at 44.8. The gap between sentiment and the markets is the widest reading in 48 years. We've spoken about this in our last two editions and it keeps getting wider. We think this is more of a survey problem than an economic problem. A trend we have come to know across many of the key datasets people historically track.

Net Net

We remain constructive. The cycle data on labor, manufacturing, and consumer spend is stable enough. The corporate side is healthy, Meta is taking share inside the AI economy at a pace that's hard to ignore if you are looking at the right metrics, on top of their 30% growth, IGV's overbought setup is historically a buy not a sell, and ChatGPT just printed the fastest adoption curve in consumer tech. The asterisk is the IPO supply lining up behind Anthropic and OpenAI. History says those baskets average -55% drawdowns in Year 1. So we keep the thesis intact, watch the IPO names get repriced post-listing instead of chasing them at the open, and stay long the franchises that keep executing.

Looking Ahead

NFP today (June 5). Revelio bounced. Now we see what the official print says. 172k jobs added.

AI IPO calendar. Anthropic filed, OpenAI on deck. Pricing and float will matter.

Industry guides coming. AI infra, data centers, semis, energy. Get ready.

That’s all for this week!

Know another investor who'd find this useful? Forward it along or share on your page!About Avory & Co.

Investing Forward.

www.avory.xyz

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn’t constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us:

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube”: Channel

🎙️ Avory: Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.