9 Charts: The rotation is starting.

AI or nothing, until it isn't.

Big Picture

💡 This week we got a tiny glimpse of what we think happens over time. The rotation seems to be starting.

This week we saw two back-to-back days where the Nasdaq was down 3% and then 2%, and our book was up over 1% on each of them. Even today as I click send, we are up 2.7% roughly as we head into closing bell, and market down. It is truly striking market behavior but indications of what we have expressed.

Over the last 24 months with political and geopolitical events like tariffs and war the market has shunned large pockets of the market. Bill Ackman this week said it best in an interview I heard…

Bill Ackman this week: “businesses with highly predictable future cash flows… are ironically where investors are withdrawing capital, making them the most attractively priced they have been in a long time “

We agree with that and we saw emerging signals that investors I mean TRADERS are on edge of the AI trade as Microsoft pushes towards open source models, Open AI delays their IPO, and Uber is gating AI token usage. This is good news.

Now it would also help to finally be done with political ping pongs so that inflation and growth concerns can normalize. Given our positioning today, that is the catalyst.

The way we generate returns is a company takes a significant portion of the cash they generate and reinvests it into the business. The investor’s ultimate outcome depends on the long-term residual value of the company. Which means it is the cash flow over the next 3-5-7 years that matters which eventually drives that stock price. That has been the lifeblood of markets for a hundred years.

This week we continued to see oil prices drop. Good news. Let’s see if that holds, seems more likely than not.

Everything about Uber and Microsoft and OpenAI chips away at the AI or nothing narrative. What you get instead is a rotation into durable, sometimes economically sensitive names that in many cases have better underlying economic stories than the AI leaders, and they are finally getting their day in the sun. It is still 6am in that day tho…

We think this keeps building as war gets pushed to the background, inflation continues heading back in the proper direction over the next several months as it should, and we work through more earnings from the companies we own and watch. AI is very real. We are looking for companies we would be happy to own for the next ten years if we were forced to hold. Most of the AI darlings today do not fit that test. Some do and we own them. If the market had to stay closed for the next 10 years would you really feel comfortable owning Micron at over $1T valuation? Not so sure about that. I feel comfortable about Block, Meta, Amazon, Omnicell and others though.

We also got more confirmation on consumer this week, which has been a constructive view of ours for a while now. The savings rate got revised up again. Q1 GDP was also revised up from 1.6% to 2.1% annualized. Same pattern we keep seeing. Government data shows one thing on release, then quietly revises in the direction of a healthier consumer and a better economy. This is now 18 months of the market fearing a consumer that, in our work, keeps showing up in better shape than the headlines suggest. Another piece of evidence behind why we keep leaning into the durable, economically sensitive names.

This week we also share a little on memory over-earning by close to a factor of 10, how Cerebras shows there is another path that does not require HBM for inference, and the fact that three of our companies use Cerebras. Then a few notes on how Meta is benefiting from AI directly. That is the tone this week. Patient, second-order, and getting a small preview of where we think this market is heading.

Here’s Latest Podcast on Meta: “6 Questions on Meta: Burden Today, Moat Tomorrow” Listen on YouTube, Spotify, Apple.

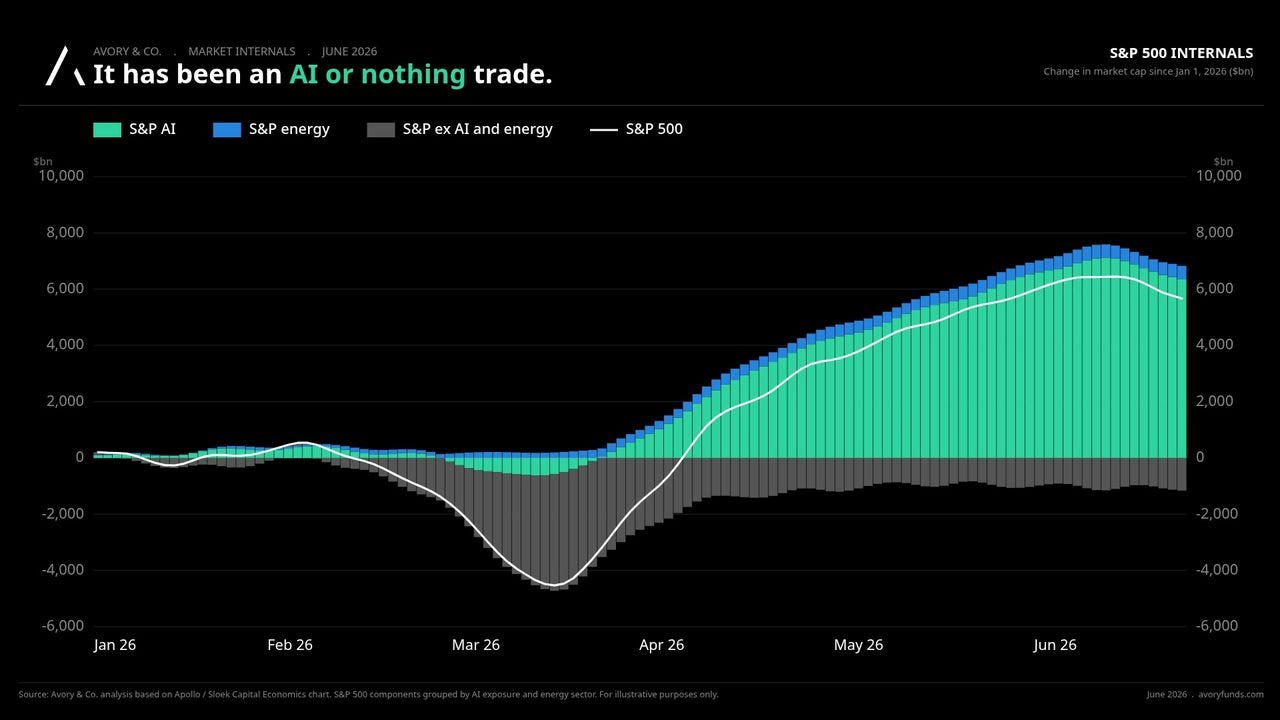

[1] It has been an AI or nothing trade.

The S&P has added over $6T in market cap this year but AI is doing almost all of the lifting (green). Energy is a small slug but that is evaporating as I write this as energy names are now being hammered as the war trade is degrossing. Two months ago it felt like you should own energy, now it’s the opposite with oil collapsing 30%. Is that trading or investing? The real take here is that the rest of the index is below zero. There’s lots of non-AI opportunities. That is the market we are in. We’ve been beating this drum for a while.

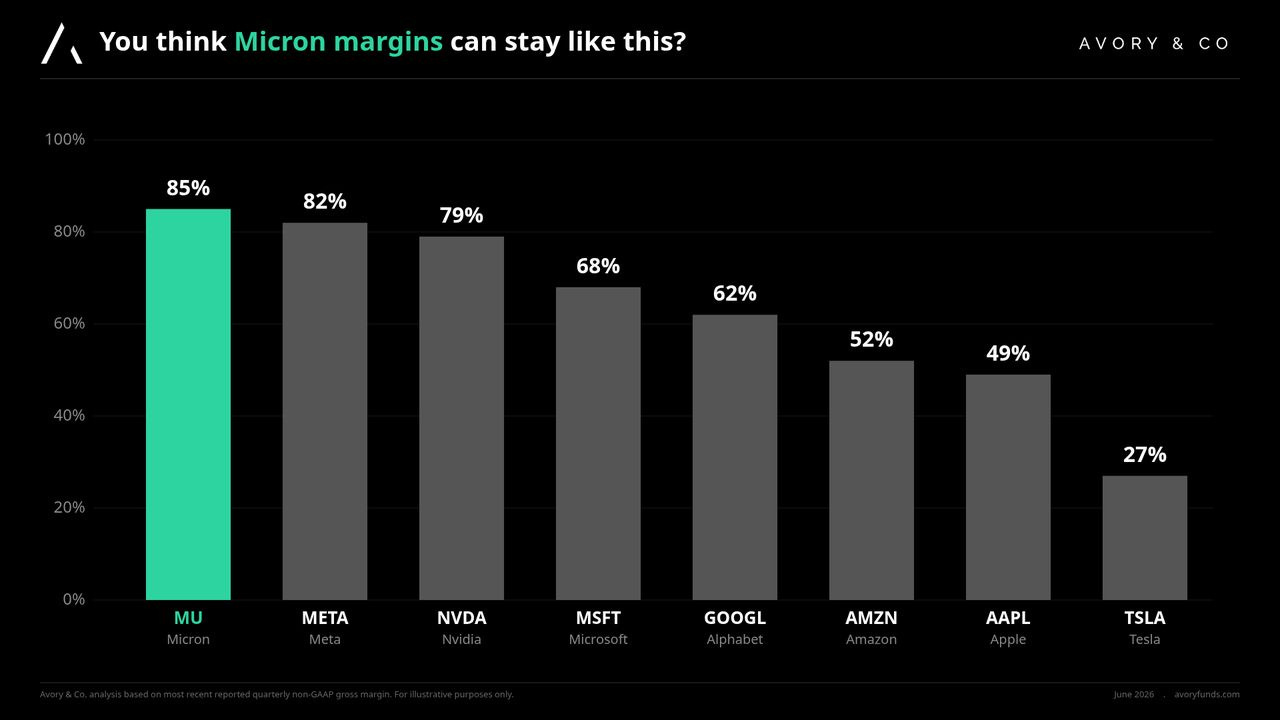

[2] You think Micron margins can stay like this? I don’t.

Micron is running 85% gross margin. That is above every Mag 7 name. Hardware has never sustained margins like this for long. Apple is closer to 30-40%. You really think Micron can hold 85% or even half that? I suspect not over time. Nvidia has averaged 60% over cycles. We think the memory complex is over-earning by close to 10x. Yes, 10x. Good for Micron, but man that is going to be such an ugly pop at some point. Revisit in a year. The cycle always shows up. Not a name we would want to own for ten years, and I will share more in a second.

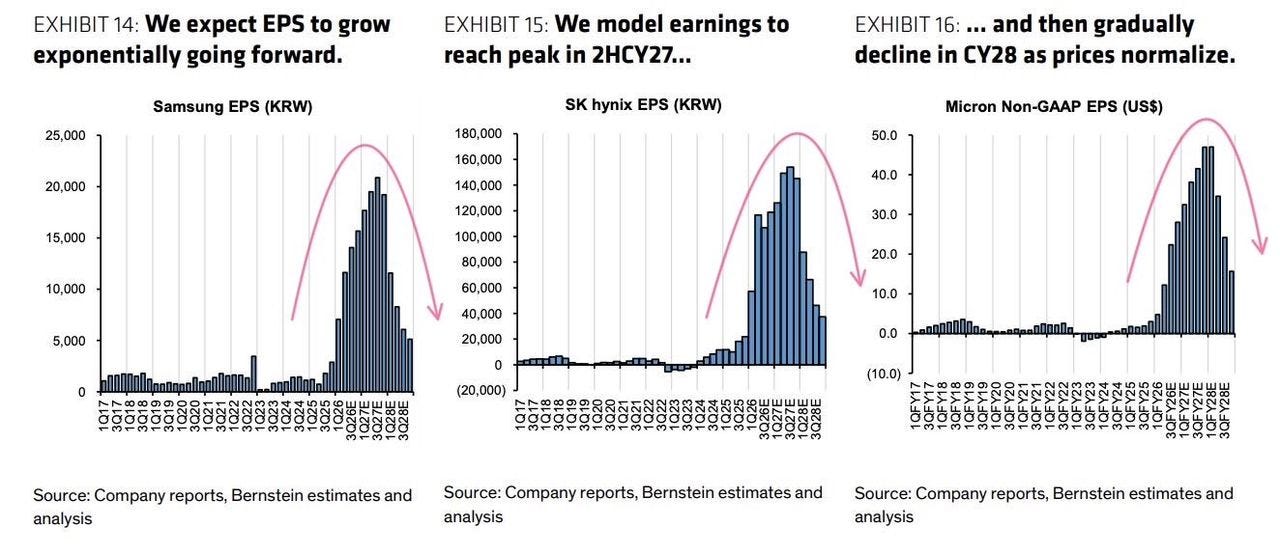

[3] Is that sustainable investing, or market timing? Like flipping homes in 2007. Don’t be the bag holder.

Here’s some numbers just to see. Bernstein models Samsung, SK Hynix, and Micron EPS peaking in 2027 and cutting roughly in half by 2028. So basically going from $500 in earnings to $20,000, then down to $1,000 over time. So the stock would essentially be up 10x on earnings that 10x’d, that looks normal. But then what happens when that drops back 70% as shown? If you are buying these here, you are timing a cycle. That is fine. Just call it what it is. We would rather compound into a business than try to nail the top tick.

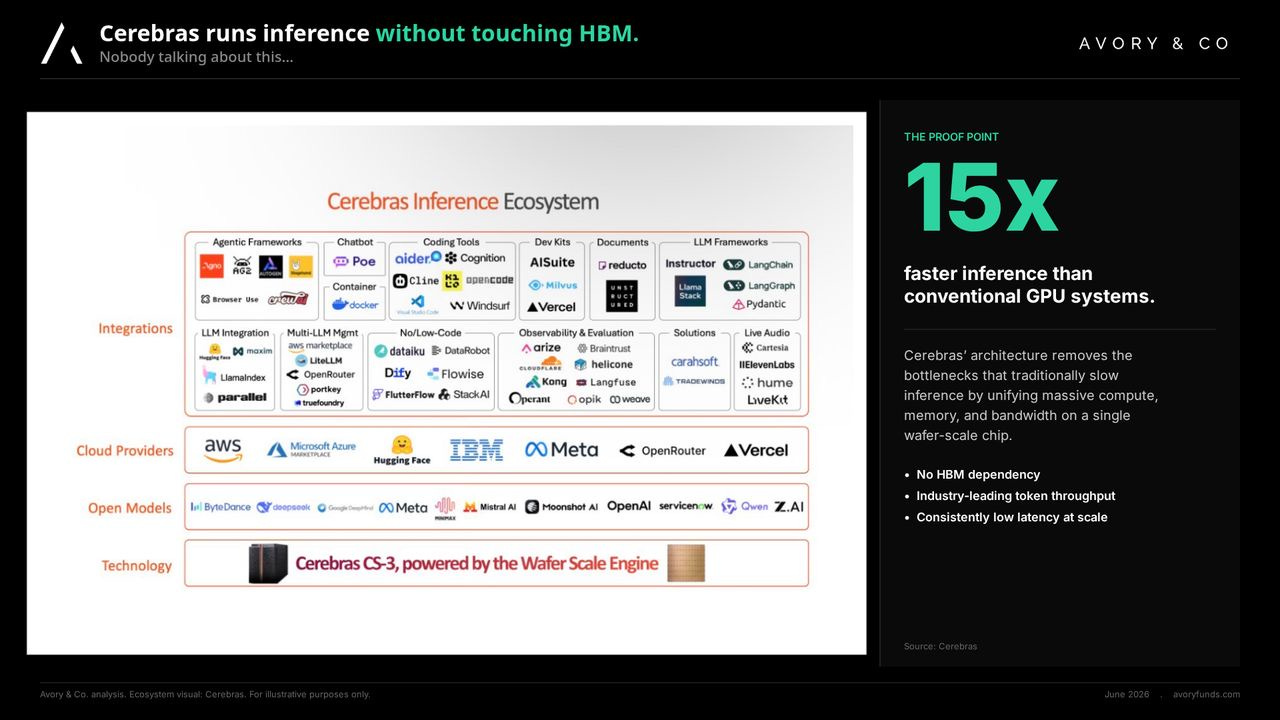

[4] Cerebras runs inference without touching HBM. Nobody is talking about this.

This one is so key. And frankly not enough people are talking about it.

The memory trade is built entirely on HBM scarcity. It is scarce no doubt, Micron revenue and margins show this.

Cerebras CS-3 is wafer-scale and uses none. You heard that. None. No DRAM/HBM. Which means inference is possible without it. Hmmmm. Also 15x faster inference at the same time. If inference really is the order-of-magnitude opportunity, that bottleneck cracks open. Another reason we’d take the cash flow from the memory names today rather than the multiple tomorrow.

[5] Cerebras counts AWS, Meta, and Block as customers. We own all three.

Three of our companies seem to be playing this right. They were named as customers of Cerebras for best in class inference and no HBM bottleneck.

[6] Meta is best in class on basically everything.

, growth (+33% YoY) and distribution (3.56B daily users)")

Now to AI and Meta. We have said they are the best way to play AI and there’s lots of reasons to believe this. I find it hard that most don’t understand this. Again, maybe because the beneficiaries are being left behind. Bespoke actually has an AI applications basket and it’s down 17%, these are supposed to be the AI beneficiaries, but still the AI builders are seeing the interest. Logically doesn’t make sense, but it may just be the short-termness of this market. For Meta: engagement, ad load, revenue per user. Meta keeps showing up at the top of every chart that matters. AI is making each of these levers better, not replacing them. This is the kind of name we are happy to hold for the next ten years.

[7] 45% of all genAI ad spend is going to Meta.

Every AI company that wants users has to advertise to find them. They are all spending on Meta. Roughly 45% of genAI ad dollars are landing there. Meta is quietly selling the shovels and the market is not pricing it that way. This is the second-order AI exposure we want.

[8] Meta AI surfaces are scaling fast.

Meta AI is now showing up across the family of apps at scale. They are their own biggest AI customer. The distribution advantage is enormous and it is compounding quietly while everyone watches the chip names.

[9] meta.ai traffic is up roughly 4x since January.

Standalone meta.ai web traffic is up around 4x since the start of the year. Nobody talks about Meta as an AI consumer product. The chart says they probably should. Another example of how Meta is winning at AI while the headlines look elsewhere.

Looking Ahead

Rotation. Watching whether the down-Nasdaq-up-us days from this week become a pattern as oil settles and inflation cooperates.

Memory cycle. When the HBM print starts to mean-revert, that is the tell on whether the cycle names get repriced.

Meta print. Next earnings will test the AI ad spend story and the meta.ai user numbers.

That’s all for this week!

Know another investor who'd find this useful? Forward it along or share on your page!About Avory & Co.

Investing Forward.

www.avory.xyz

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn’t constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us:

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube”: Channel

🎙️ Avory: Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.