Q&A + Letter: Five Questions for the Second Half of 2026

Our 2H Avory Views

Three things:

Avory Letter = contributors + detractors + companies we are watching: Read Here

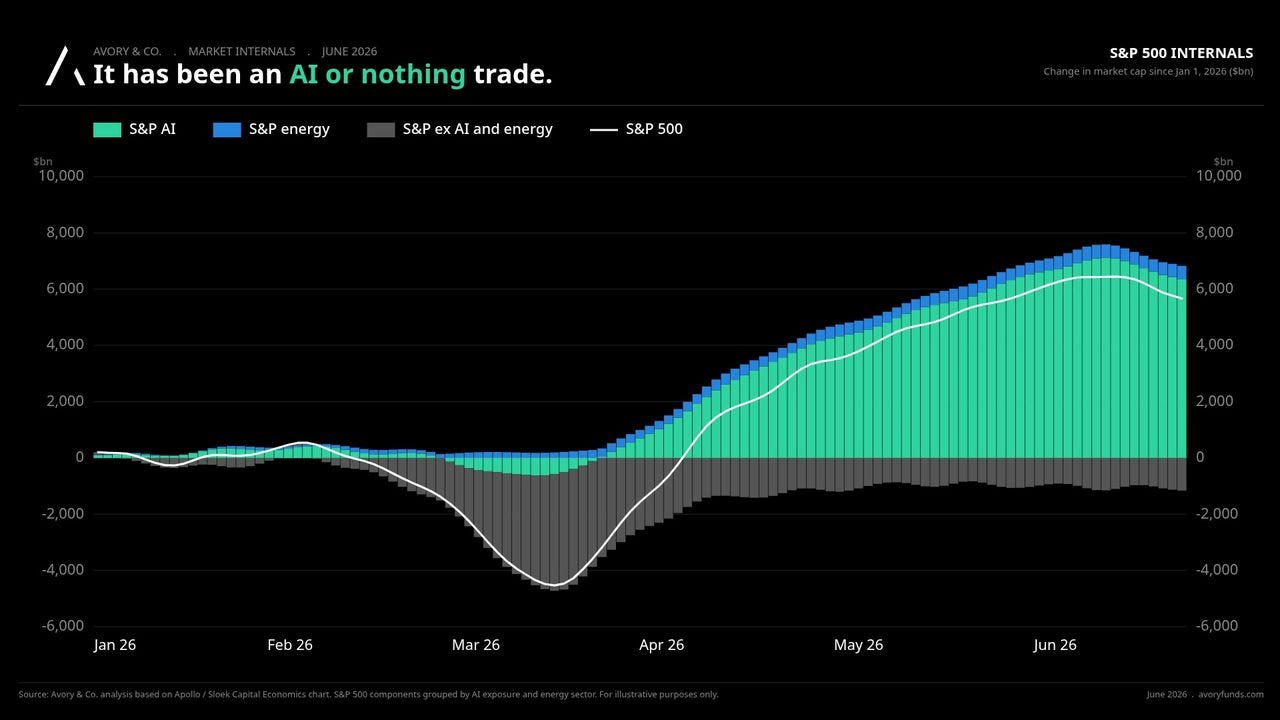

Here are some additional charts we wanted to share as we head in 2nd half of 2026.

AI is driving markets, but rotation is happening. Markets have gone through two very disruptive phases over the last 18 months. The first was tariffs. The fear was straightforward: tariffs would push inflation higher, the Fed would stay tighter for longer, economic conditions would weaken, and the consumer would crack. We did not fully buy that view. Our view was that tariffs were disruptive, but the way they were structured and phased in would not create the same inflation pulse the market was pricing in.

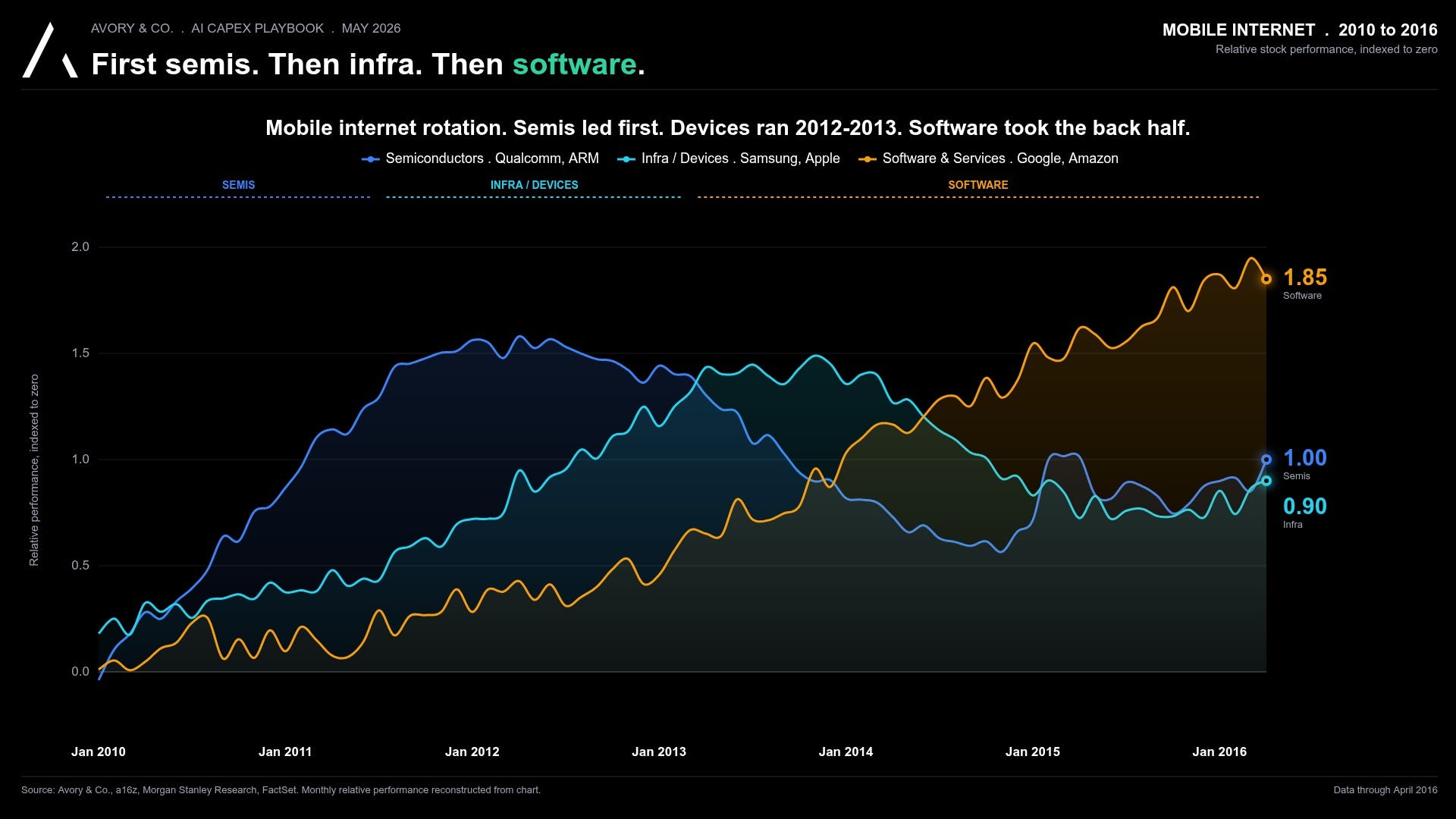

This image is in the letter but I want to reemphasize it because it speaks more to opportunity then anything else.

Every is focused on AI infrastructure for good reasons, but below shows where value accrued during mobile / internet cycle. We went from infrastructure to applications. That is where value is created. How you use it, not how you build it.

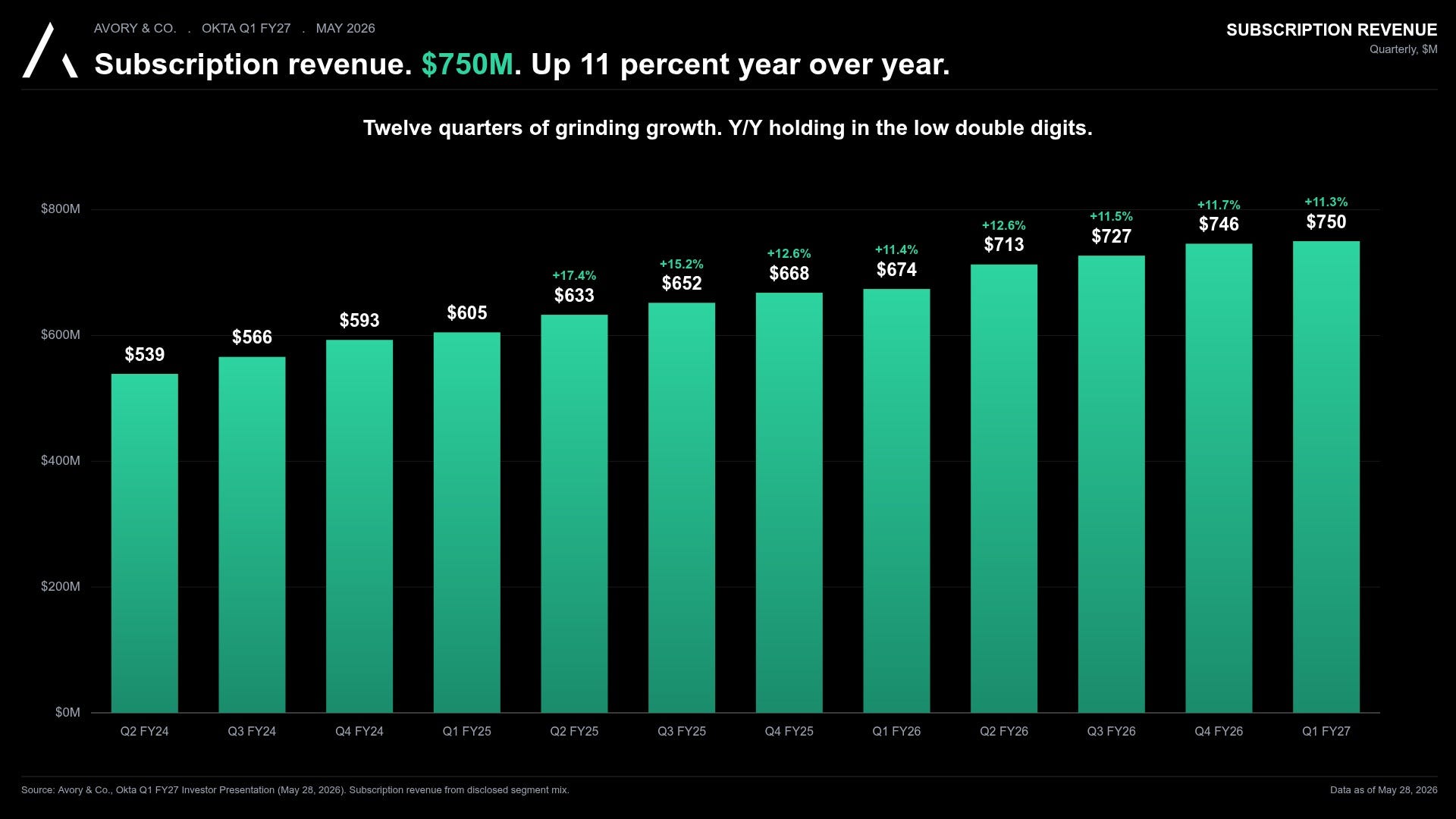

We highlighted Okta in our podcast and the letter. It was +73% in the quarter which helped as their Agent Identity backlog is growing. Again value accruing to applications. They will not be the only ones.

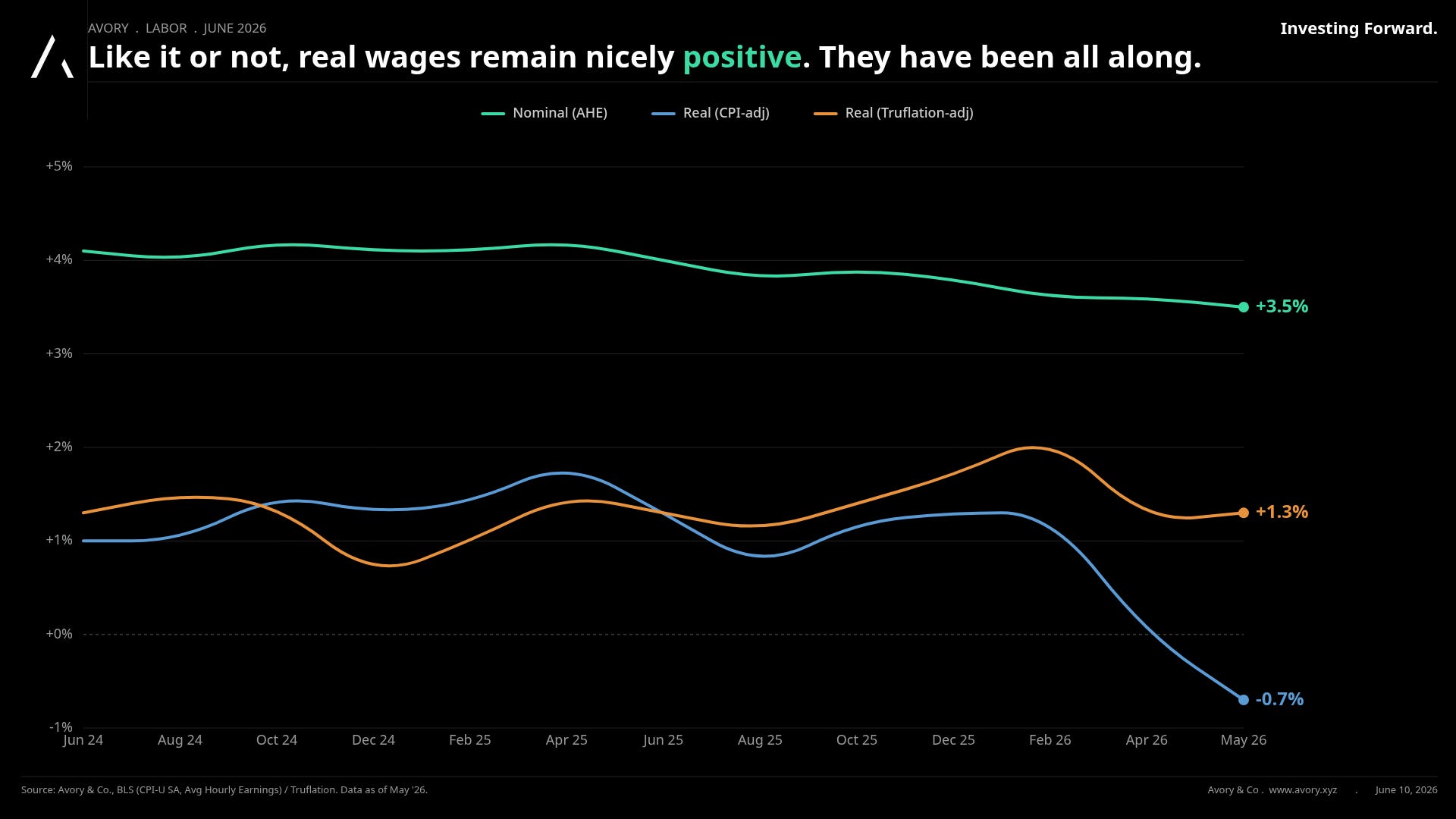

Just a reminder that consumer spending should remain supported by positive real wage growth. The broader backdrop is still constructive. If the administration can reduce the uncertainty it has been creating globally, that would likely provide an added tailwind for consumers, businesses, and markets.

That could also help names like First Watch finally get some sun shining on them. The company had a good quarter, and momentum appeared to improve toward the very end as ceasefire discussions and announcements helped ease some of the broader macro anxiety.

And if we take energy futures curves and roll them forward, the setup increasingly supports the idea that we have already seen peak inflation pressure. That matters because easing inflation pressure helps support real wages, lowers the fear of additional rate hikes, and improves the backdrop for consumers, businesses, and markets.

That ties directly into what we discussed above. Positive real wage growth plus easing inflation risk creates a much more constructive setup for consumer-facing names. More on that in the full letter.

Software wants to jump. On one side people are nervous, on the other side people see opportunity.

This isn’t our weekly newsletter piece, so stay tuned for that later this week.

Have a great Fourth of July! In the meantime, check out our latest podcast episode and read the letter.

Again here you go!

Listen to our quarterly Q&A here: Click platform of your choosing

[YouTube or Spotify or, Apple]

Avory Letter = contributors + detractors + companies we are watching: Read Here

Know another investor who'd find this useful? Forward it along or share on your page!About Avory & Co.

Investing Forward.

www.avory.xyz

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn’t constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us:

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube”: Channel

🎙️ Avory: Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.